Maybe some of you have heard about Vilfredo Pareto or the 80%-20% law.

Mr. Pareto in the beginning of the 20th century observed that roughly 80% of the land in Italy was owned by 20% of the people and that a similar proportion was valid for the other countries. As of today this unequal distribution is more and more valid (some studies show that 40% of total asset in the world are owned by 1% of population).

The same law applies in business; usually 80% of revenues of a firm come from 20% of the customer.

How does it apply to our life?

Think about the results (positive or negative) you got from your life (personal, business).

Can you see the correlation?

Every day, every morning, focus on the 20% causes that produce 80% of your results; put more attention on the positive 20% and eliminate the negative 20%.

In my case I noticed that keeping an open mind and networking actively and sincerely (really caring about people and co-workers) made me found very good job opportunities (other people offered it to me, I didn’t even need to searching it) that I would never found just sending resumes around (80% of efforts!)

Me after the job offer

On the negative side: exercising and kicking 1-2 small bad habits produced a great benefits on my health. Moreover; complaining (How to stop Complaining for good in 9 days) creates more than 80% of the troubles and limitations in our life.

Eliminate it right now!

We need to deeply understand what is really important on our life and focus on it. This would mean to cut some activities at work (some people will complain but stick with the principle) or sacrifices (cutting TV is an ideal!).

But I can assure the results will be astonishing.

Wake up with a crystal clear picture of what it really matters and work on it; eliminate the inessential and reach your goals, the one that really matters.

First Things are the most important things for your life; the only ones that really matter.

Typically First Things are:

Exercising

Actions to reach personal goals (whatever they are)

Saving and Investing Money

Spending quality time with your family

Educate yourself

Finish (excellently) all the tasks at your job (if you have one)

That’s it…nothing more…nothing less.

The rest is only noise.

Instead….

How many times did you schedule to exercise (How to avoid to die young) after work and inevitably skipped ?

Work is an insatiable animal, it devours our time; the last call or email typically takes 2 hours and we end up leaving the office at 8.00pm. So long exercising or read that book that sits on our night table for 1 year!

What you need to realize is that everyone wants our time and moneyand most of the time exclusively for their benefit.

Saving money is the same (The 3 simple habits to Reach Financial Freedom) ; if you wait the end of the month saying “I will save what I will not spend this month” very likely you will end up saving a lot less (if zero) than if you had immediately (after you got your paycheck) transferred some money to a saving account.

You and me know right…?

Instead….

You need action, focus and discipline

If you start our day scheduling the “First Things” we will be sure to move on in life.

Don’t do like this guy…(yes I love him…)

This means waking up before everyone else and setting up 2-3 hours to complete the tasks.

Reading or writing that book (or blog) or concentrate on your next business with kids, wife or peers around it’s impossible; you need to find a timeframe for yourself alone.

Yourself alone.

Not everyone is a morning person, I also experimented working late a night (when everyone was sleeping) , however I reached the conclusion is better to complete the “Thirst Things” in the morning.

Typically (unless you are very determined) it’s difficult to always leave work at 6.00pm to go to the gym, or schedule to work from 10pm to midnight.

Your job, peers, kids or wife will put a lot of pressure to get also that timeframe.

Early in the morning there is no that risk; you will have 2-3 hours for yourself.

I understand this translates in waking up before 600am (I wake up at 530am shooting for 8 hours sleep) but it’s a sacrifice to get your life back from the madness of the day, where everyone wants a piece of you, often for not important (at least for you) issues.

They must be the most important two hours of your life, necessary to refocus, giving a direction to your life.

You must see these 2-3 h as the timeframe allocated to stretch your comfort zone (The most dangerous place to be!); the rest of day must be dedicated to enjoy the, this time, valuable comfort zone you created (with kids, wife, in the hopefully nice place you created).

Roughly one year ago I started this blog with the main purpose of writing and sharing my experiences.

Nothing more, nothing less.

Then I started reading similar blogs on health, personal development and financial independence.

I noticed that Many Financial Independence blogs were publishing their revenues associated to ads, affiliated program and various products (e.g. eBooks, courses) etc.

Intrigued by this I started putting together something similar and…believe me…uniquely pushed by the curiosity that it is indeed possible to monetize the blog.

Well…to my misbelief you can and big time:

What I did

Amazon affiliates

Link to my favorite books and products.

After a couple of months of zero revenues somehow the revenues picked up.

Time to Set it up: 1h Average revenues per month at March 2019: $8,000

Adsense

I don’t like too much this method because it doesn’t give me a lot of control of the ads I am publishing but Hey…it works!

Time to Set it up: 1h Average revenues per month at March 2019: $$6,000

Ebooks

I wrote a couple of books (not big revenues here…I think I have to improve my writing skills). That’s also the item where I spent more time with smallest revenues.

Many people spend most of their time working in a job as an employee.

If you spend most of your live doing one thing you better love it.

Otherwise you are wasting our life

And the bad news is that you have only one life.

But many people hate their job and they stick with it because they think they cannot do or deserve anything better; in a word: because of fear of change

This is the fastest path to misery and this is why many people today are, well… miserable:

Poor

Sick

Sad

Mentally limited

Stressed

Small inside

Selfish

Yes…just because they don’t like their job?

Am I exaggerating?

Really?

If you spend 8-10 hours a day in a place, with people and doing something you hate what do you think is the effect on your body and brain?

Something negligible?

Open you eyes.

Understand that, NO, it’s not normal to have a miserable existance because everyone has it in a miserable job surrounded by miserable everything.

If you are not happy in your job I am not suggesting here to drop it and just run away (even thought I am sure you will be better off than in your present situation).

And this is not an option for somebody like you who decided to be happy (as I hope you did if you are reading this blog).

You must love your job

What is important to understand here is the verb: must.

Hating your job => hating your life => you must change the game.

You don’t have any other options.

“But I really hate my job“, “It is impossible to find a job I like” , ” A job it is only a way to bring money home!”

….I know your comments…

“But I really hate my job”

In life we avoid what we hate in 95% of the cases.

We don’t eat that dish or buy that car we hate.

The decision is up to us.

So ask yourself why you picked that job that you hate.

I doubt that somebody pointed a gun to your head and forced you to accept that job offer.

Very likely you studied decades to get the qualifications of that job.

Very likely you were very excited when you got that job offer.

Very likely you are the one who designed all this.

You built the cage that is trapping you now.

Ask if you hate your job from the beginning or the initial enthusiasm faded away.

Ask yourself why it faded away and how to renew it.

What changed in your job? The job? You? Both?

Don’t leave any of these questions unanswered.

Changing job is perfectly normal, you indeed need to change it once in a while.

Hating it is not normal.

“It is impossible to find a job I like”

Sure, but…do you know what you like?

Even if this question sounds trivial (” Of course I know what I like!” ) it is not.

If you really know what you like (what you really like… 21 Minutes to Learn How to be Happy Doing What You Love) and you are not scared to attain it you will work toward that goal, consciously or unconsciously.

But if the fear prevails, you will be stuck in a job you don’t like.

You will discover that what you really like it’s not necessary laying on a beach or partying all day long but something more meaningful.

And you already know it, you laid down on that beach and partied long enough to get bored at some point…

Find what you like, let the fear go and take actions!

” A job is only a way to bring money home!”

Yes, a job is a way to bring money home and very likely you need that money.

But:

1) If you really need that job to bring money home you need to do your best to like it !

2) Again, there are plenty of jobs you can like, You don’t need to be stuck in a 9-5 hell,

Even if you don’t want to change your job because you cannot find another one with a better salary now, this strategy doesn’t pay off.

In the long run if you are doing a job you really like the results will be better so the money.

I know it for sure, I followed the money twice in my career and it didn’t pay off, at all.

So, please go ahead with clear objectives; what it really matters is:

Your job description

Your boss

Job Location

Money

If you don’t like one of the four your job will become a hell, so your life.

Without clear objectives and passions you are just squandering your life.

Especially if you are young, follow the passion instead of the money.

As I mentioned, I once made the mistake to accept a job I didn’t like but with better salary than another one I liked more.

Believe me, I am still paying the consequences for such mistake.

Had I followed my passion very likely I would have had a faster career path and more satisfactions.

It’s all in the passions, in what we really like.

You will be never successful in a field or position you don’t like.

In your job always give 110%. Always, also if you don’t like it.

This is the only way to get advanced (why should you get a promotion or more money if you are just doing your job?).

This is the only way to be fair with your employer (yes it matters!), for your professionalism and dignity.

In every realms of your life always give 110%, adopt that as your lifestyle.

Always give an outstanding commitment in everything you do; no matter your job, exercising, loving your wife or getting things done.

This is a great habit to cultivate, all your life.

Human beings like every other living species are made to use their body daily.

In a word…at least to move it…

But still….think about the life of most of us today: getting on the car to go to the office, 8-10 h glued at our desk on the computer, back home in the car, couch, bed…repeat.

Physical inactivity may increase the risks of certain cancers.

Physical inactivity may contribute to anxiety and depression.

Physical inactivity has been shown to be a risk factor for certain cardiovascular diseases.

People who engage in more physical activity are less likely to develop coronary heart disease.

People who are more active are less likely to be overweight or obese.

Sitting too much may cause a decrease in skeletal muscle mass.

Physical inactivity is linked to high blood pressure and elevated cholesterol levels

But you already know it…right?

And often when I ask “Why don’t you exercise” the classic answer is I don’t have time! Again and again, the only way to have time is to make it and stick with the schedule . You don’t have time for exercising but easily you can allocate everyday 2 or 3 hours to surfing the net or watching TV!

Exercising must be in your schedule for many reasons:

1) Decrease probability of contracting most diseases 2) Losing Weight 3) Feeling Generally Better 4) Getting Energized 5) Reducing Stress 6) Meditation moment 7) Good way to listen to your preferred music or podcast 8) Great Example for your spouse or kids

Just do it

Schedule a timeframe and a plan and stick with it. Pick whatever sport or exercising you prefer. Personally I like walking, running and fast weight lift for the major muscles (in many Gym they have room dedicated to this Express Circuit where you makes 2 series for about 30 min).

If you never exercising before start small, and increasing over the time.

Take a personal trainer if you really needs a motivation, however on the Internet you can find many blogs of schedule, training and also people in your city hanging around to exercise together.

In my case exercising comes pretty natural because I love doing it.

But what if I absolutely hate exercising?

Here is the bad news: you must do something for your body, that you like it or not. If you absolutely hate physical activities at least walk.

Walking (or running) should be in every training program. Walking at least 30 minutes a day is mandatory to keep the body active; you should never forget this. We are human bodies machines and like every machine we need to keep basic functions and walking is one of them.

The successful warrior is the average man, with laser-like focus. Bruce Lee

Be like him…

Do you control life, or life controls you?

If you are focused on what you do you control your life. Otherwise life controls you.

To be really focused is one of the most difficult achievement in life.

That’s why so many people fail to get what they want.

You and me are the people….you know what I am talking about.

To be focused it’s a habit that requires a lot of commitment, time and…well…focus.

So, why it is so difficult to be focused even thought we recognize its importance?

First of all not many people are aware of the power of focus.

It’s part of the human nature to lose focus, to get distracted.

Usually the most we like the task the most we can keep our focus; but most of the times we still need to be concentrated.

Make this exercise, whatever you are doing (a report, writing, eating) try to focus only on that activity for 20-30minutes.

Difficult, isn’t it?

How many times we started writing that email or report and by the end of day it is not completed yet?

So the tasks cumulated, we stay in the office until 800pm and we have the impression that nothing got done.

Well… actually because you really got nothing done, because you wasted your day losing the focus, switching to another activity, losing again the focus and switching again.

Think about it, the huge amount of time you waste during the switching. Be real, you cannot spend one day just answering some emails and writing 1 page of report.

Typically because after 5 minutes you are working on the report you jump to another email, conf call, browsing the news and check out the latest news about Ronaldo Girlfriend…

Ok…I let you now to lose the focus for 14 minutes and watch the below video…you will find yourself there…

Back?

Good…

Focus gives direction to your life

Focus is essential to get the things completed and in the right way.

Focus is essential to put the right attention on what you are doing.

Without focus our life is jumping from one task to another, without direction.

And without directions you cannot go nowhere and get anything done.

To achieve things and create value you need focus. If you want to play an instruments or read an essay you need to allocate time for it and just being focus on it.

Don’t think that if you don’t get the right focus on something it necessary means you don’t like it. (Generally because when you like something time flies doing it).

I love running and writing but I still need to be very disciplined to allocate the time for these activities.

I love running but I can tell you that most of the time I would rather stay in the bed than hitting the road at 5.30am in a rainy day.

But once in the run…it’s fantastic, the focus and the pleasure it’s there. The same for writing and in general for everything I love.

Again, don’t be deceived about identifying your passions in watching TV, playing games or surfing the web because when you are doing it “time flies” and you are very focused.

When you watch TV, play games or browse the web time flies because your brain is off as a result of the very addictive nature of those things.

Those things are highly addictive like alcohol, drugs and tobacco.

Just look around you people literally glued on their phone if you don’t believe me…

Practice focus

The new you

Practice focus: start small, on the daily activities: when you eat don’t watch TV or be on the phone, just eat; when you start an email just don’t do anything else until completion. Let the phone ring (unless it is a very important customer or a real emergency) and check the voice message later.

Commit 10 min of focus on one activity and gradually increase to 15-20-30 minutes. The goal here is to allocate a timeframe for an activity and complete it in the decided timeframe.

Thirty minutes for a report, 30 minutes for emails , 1 hour exercising etc. with no interruption.

By the end of the day the results will be astonishing: the important report completed, the inbox clean and your workout done.

Be beamed focus in everything you do; you will reach your goals and the world will be yours!

“The pessimist complains about the wind. The optimist expects it to change. The leader adjusts the sails.” – John Maxwell

Make a favor to yourself: stop complaining,

Right now and forever.

You cannot?

Ok so keep reading…

Complaining is the worst thing you can do to yourself.

If you spend most of your time complaining of something it means you need to change that something.

As simple as that, otherwise you are going nowhere.

Complaining is not changing a situation, it just aggravates it. This because you are putting focus on a negative situation and what you put focus on it expands.

As human beings we need to find solutions to problems, not problems to situations.

Finding the problem is easy, it’s the 5% of the job.

Everyone can step in a situation and find dozens of problem in it.

The value is to bring solutions to problems.

Complaining you are fat will not make you lose weight.

Eating less and moving more will.

Losers find problems to solutions and complain.

Winners find solutions to problems and prosper.

It is up to you to decide on which side you are.

Why people complains?

Most of the people seem stuck in their lives, jobs, marriage, situations, etc. and they complain all the time.

Why ?

I came up with four main reasons:

Family

Fear of Change

Sense of unworthiness

Because it’s the Easy way

Family

Some people prefer compromising (e.g. a job or partner with few/no satisfactions) rather than disappointing family members.

In some case the compromise can be acceptable (for example not taking a job abroad to stay close to family members).

But, most of the time it’s an excuse!

They use the Family card to complain and justify the reason why they don’t make enough money or why they are not courageous enough to bring some changes in their lives to live in their Dream location doing what they love.

Fear of change

Fear is the number one obstacle that prevents people from growing.

Think about it : almost every personal improvement goes through some degree of fear (learning how to swim, sky, or to change for a better job/place).

Basically for two main reasons: not leaving a comfort situation and for reason number three: sense of unworthiness.

Sense of Unworthiness

Often we resist change because we don’t think we are able to achieve things in life (“to be unworthy”).

“I can’t ever do that job!”

“I cannot learn how to sky!”

“Only big bosses can get a VP position”

…you know what I mean.

So instead of trying the take big leap we decide to stay in our condition certain that this is the maximum we can achieve in life.

This behavior comes from of our society that inculcates a strong sense of modesty and negativity.

Having spend my life in different Countries and Continents I was able to experience the strong influence of the society on its people.

Usually the development of a Country depends upon to the degree of positivity and hope of the society.

Many people just don’t grow because they are negative, they don’t believe in themselves because they were thought in that way .

They spend their time complaining and their society is characterized by conflicts.

Conversely, where union and positive attitude are predominant, people are growing, intellectually and economically.

Complaining is easy

Again but why it looks like everyone around us is complaining?

Well, because people are (for some reason) negative and moreover because complaining is easy.

Yes, complaining is the easiest thing in the world.

Think about it, complaining can justify your failures in every situation, job, relationship… in everything.

So, is it easier to wake up and improve the situation (or simply accept it) or just complaining? Complaining it’s your boss, partner, friend, family, the weather, the economy, , etc. fault?

This is exactly why people spend their time complaining. It easy and justify our failures.

That’s why you are going to easily see people complaining about their boss while they take their thirty coffee break instead on working on improving the quality of their job.

If you don’t like a situation work to change it.

Don’t stop until it change.

And it usually works if you are really focus and convinced to change it.

When you don’t like a job or boss simply change it, it easier than you think. You of course will go through a slight disconformable period due to the changing process (disrupting your Comfort Zone) but you will find a solution to a problem.

I know many people are thinking now “You picture it too easy; it’s impossible to find another job”.

I can tell you it easier than you think; I made it several time through my life and now I am happy.

But you really need to face the situation and win the fear of change.

There are billions of jobs, partners, places and situations out there.

Better than what you are experiencing now.

Don’t just sit and complain about your situation stating it’s impossible to change and trying to show the world it’s not your fault for the failure.

We are the only one responsible for our success and failures.

For sure some external factors can influence some situations but only marginally and very temporary.

All the decisions we made are up of us; our jobs, partners, friends, health and wealth.

Everything.

How to stop Complaining for good in 9 days

Make this exercise, I promise you it will be very illuminating.

Stop complaining for 9 days.

Only 9days.

Not only externally but also internally, mentally.

Whenever you feel like complaining just stop, think about something else, tell yourself you will complain later, at the end of the 10 days.

I promise you: after the 10 days you will see the whole world from a different angle and start understanding the negative power of complaining.

And the great power you have inside of you, if you just want to use it.

Again, make a favor to yourself and the whole world stop complaining and aim for the excellence.

I don’t have blocks on what I love, you should have not either.

I can, right now write for hours, days, months.

Maybe not like Hemingway but like me, talking about what I love.

If I have to write about what I love, this comes natural, fluent, because I have tons of things to say..and I want to see all of them.

That’s why the Writer Block simply does not exist.

If you are blocked is because you have nothing to say, you are not interested in the topic.

If you love playing tennis, you will play it. If you are not playing it right now is simply because you don’t like it, not because you don’t have time or your body cannot.

Same for the writing (or speaking)

We should write because we have something to say, not something to fake, to build up to meet our audience, because we need readers.

We do need readers because we do want to be read but, first and foremost, we do need to have a message to convey, to share, to debate.

A message that ignites something in your readers, that makes them think, wish to be better, or simply create a small revolution inside their soul.

Money

I know I know…already seen…but I love this pic

We discussed about it.

How to save them, to invest them…to reach financial independence (if this is what you want)

Then what?

Retire from you bad and evil boss…uh uh poor you…

And what you are going to do with all that saved time ?

Listen, if money is the only thing you are looking for and blogging is what you think is the solution you should stop write now writing and reading the tons of blogs bragging they make hundreds of thousands of dollars per month.

Yes you can make money blogging.

But

You must have some good message to convey (otherwise why should I read you

You must have some fundamental on how to market you blog

You must have sincere interest on other similar blog and interact with them

You must put the work…real work

Or

You can get a job to flip burgers and be sure you can make more $$$-hour.

Excluding some exception of very first comers (but with very strong valuable messages like Steve, very hard workers (100+h/week like Michelle) , mediocre blogs who were able to get visibility on top 10 blogs worldwide (too many unfortunately) not many bloggers make tons of money.

Just relax

Just write what you really believe in.

What you would like to talk for hours, days…

What you would like others to listen.

From suggestion on investing in mutual fund, to how to build a giant castle made of Play Doh.

It doesn’t matter the topic.

As long you write about what you love and convey a valuable message.

Enlighten other people with your gifts. your achievements, your energy.

Open their eyes like many other blogs, books, magazines, websites, people opened yours and mine and changed us forever.

How many of you are still following that fantastic 500 calories a day diet no fat, carbs, sugar nothing…?

How many of you already lost tons of Kg, stones, lb etc etc?

None right…?

Ok…we are talking now…

Why diets are not working

I am not a dietologist or an expert in the field.

What I can tell based on my experience is that I tried many diets, I am in a pretty good shape (normal weight BMI even thought I was lightly overweight for a couple of years) and I read a lot of books, articles, whatever on the losing weight topic coming to 3 conclusions:

1) Diets say everything and its contrary.

Eat low carbs….no low fat…no low sugar…skip lunch…I mean dinner…no beer only wine…I mean only red wine…pasta yes…pasta no…mediterrean diet is great…wait but bread is not good…only white rice diet…the nutrition pyramid is the mantra to follow…well but so many carbs etc.

Ad nauseam

Have you ever wondered why there are so many theories and buzzs around losing weight?

1) Food packaging, transportation, fertilizer, infrastructures, real estate, (btw do you know that the real business of Mc Donalds is Real Estate and not burgers)??? , commercials etc.

2) Health care related to food. Abuse of food generated diseases…diseases generated trillions of money to treat them.

3) Gyms. Most of the people going to Gym is there to lose weight. No fat on our waist no big dollars in Gym owners.

4) Dietary Supplements for weight management: zillions of dollars spent every year in those products (I wonder with which results…)

2) Relying only on Calories Balance is wrong

Use calories in a correct way

How many times did you hear the following equation ?

Calories In = Calories Out + Exercise + Weight Gain

It seems simple…making sense.

Eat less, move more and you control the weight.

This is only a part of the equation.

This because not every calorie is the same.

Or better…not every calorie has the same effect on your body:

e.g. a calorie you get eating an almond is processed differently by your body vs a calorie you get from carbs like bread)

Additionally reducing Calories In has a direct impact on Calories Out because our body has the natural tendency to reduce the Calories used (Calories Out) in case it starts receiving less Calories In (it’s a natural process of avoiding starvation and death).

I don’t want to go into the details since I am not a Doctor and the argument is long and complex but I might suggest you some interesting reading from Dr. Jason Fung like The Obesity Code and The Complete Guide to Fasting.

Again, I cannot say Dr. Fung Theories are the Undeniable Truth but they do give a different interesting prospective on diet, food, diabetes and some common mistakes.

I personally used some suggestions like Intermittent fasting and I got benefits both from general feelings (e.g. more energy, less bloated) and losing weight (2-3% of my original weight..again I was not particularly overweight when I started).

2) There is too much emphasis on exercise and not enough on resting.

Do you sleep enough?

Exercising seems the panacea for losing weight.

I have a bad news…it’s not.

It might help but it is not.

In one hour run (that I am pretty sure you don’t do it daily) you are going to burn around 600-700 Calories.

Half an hour and it drops to 300-350 Calories.

Considering now the total budget of 2000 Calories for someone who tries to control his weight.

Three hundreds calories are 15% of the total. (20% if he is on a 1500 Daily Calories budget).

Or…do you know how many calories there are in one pizza?

Roughly 820 calories (yes you would need to run for 1h 15min to burn it).

Drink two beers (230 Calories) or a couple of glass of wine and you just drank your run.

Watch out I am not saying you don’t have to exercise.

You must on the contrary because exercising have tons of benefits.

I am just saying that the contribution of exercising on losing weight is much less than you think unless you run very long distances (marathons or ultramarathons (I can tell you based on my experience that when you run 50-60 miles per weeks (90-100Km) you definitely lose weight).

What about resting (sleeping)?

Everyone associate sleeping as a synonymous of laziness.

Executives shows their budget of productivities claiming that they sleep only 4 hours per nights!

What losers…

Sleep is an important modulator of neuroendocrine function and glucose metabolism and sleep loss has been shown to result in metabolic and endocrine alterations, including decreased glucose tolerance, decreased insulin sensitivity, increased evening concentrations of cortisol, increased levels of ghrelin, decreased levels of leptin, and increased hunger and appetite. Recent epidemiological and laboratory evidence confirm previous findings of an association between sleep loss and increased risk of obesity.

Similar study are everywhere out there but nobody is talking about it?

Why?

Lack of Money.

There are no money surrounding the statement Sleep more (and without pills or whatever external help) while there are tons of money around saying Do that and buy my products in the process.

If you are still unconvinced I suggest you a great book on the importance of sleep:

Below is quick look at the Professor and his theories on other benefits of sleeping (and the damage of lack of it).

So what now?

Are you confused?

Losing weight is a complex equation that involves:

What we eat,

How much we eat,

How much we sleep,

How much we exercise,

When we eat.

Society is pushing toward an exaggerate diet mostly based on highly processed carbs with the results of an epidemic of obesity.

Conversely (especially in the USA) we see people eating low fat diets , new gyms popping up everywhere, many people panting trying to reach the 10,000 steps on their brand new bracelet but we see those same people severely overweight and dying of hearth attack or developing diabetes 2 in their 40s.

There is something wrong here…and usually when you cannot find a logic answer to a solution just follow the money*…

Did you follow the money?

Good…

Here are my suggestions:

Watch out the Calories In-Out balance (I personally use and love the App MyFitnessPal (free with some Premium features) . This is one important step but not everything.

Drastically reduce carbs like bread, pasta rice etc. and highly processed food.

Eliminate white sugar as much as possible

Exercise seriously (at least 1h 5 times of weeks of aerobic activity)

Try some intermittent fasting to regulate the insulin in your body (e.g. 16:8 or more aggressive Warrior Diet).

Read Read Read. Try to get some exposure to books, article, researches from independent and entitled professionals. The mantra here is Do not follow the money.

Track your weight daily: where you focus results appears…Don’t forget to track your weight for one month and discover you are 10 lbs (5Kg) heavier.

If you can eat at home. Not only you will save a lot of money and learn something fun but you will drastically reduce the processed food you ingest and improve the quality of the ingredients.

*Let me ask you…what is the food with highest content of Vitamin C in the world…the Orange right…? That’s what most of the people think but it’s not true…have you ever wondered why?

COMMENTS

Not very active but I am not very surprised since:

1) Traffic is still too limited

2) Most of My blog posts doesn’t really leave a lot of room to comments, questions

3) I think people prefer to comment on twitter, facebook etc instead of directly on the blog

I am not surprised the Blogger Dilemma reached the top spot since with the proliferation of the blogs more and more people are somehow disappointed and disillusioned from the lower than expected traffic in their blogs. The post brings back on the basics: i.e. creating value. The post in second place very likely had several visitors trying to understand what the blog was about. I have to say I was not surprised of the post in third position since most of my readers seems attracted by topics such retirement, where to live and they are from the U.S.A.

In late November I started the Twitter account linked to this blog and I am having a blast to read all the interesting comments and post of my fellow bloggers out there. In few weeks I was able to reach over 100 followers (20% in my opinion are only real followers). I also opened a Facebook account linked to this blog but I do really think blog + Twitter is enough so far as main communication channel.

WHAT IN 2019

1) Publish every Saturday no matter what 2) Start some experiments in monetizing the blog 3) Extend to other social channel (e.g. Instagram, Reddit, Pinterest) 4) Being published by some media 5) Reach 10K Visitors/mo 20K Visits/mo

While always (trying to) create some value for you.

I found that people are trapped in their habits (often bad) due to the most two dangerous status in the world…

They are comfortable.

Ironically comfortably enough is the main goal for many people.

A roof on the head, enough food in the refrigerator, a nice tv, car and sofa.

What do you want more then right?

Well if you are one of my fellow readers you want more right? (otherwise you would be (again) comfortably browsing the tv on your couch instead of browsing blogs on personal development).

Let me state it straight….most people love to be comfortable…9 to 5 until 65 and ending their life in a nursery home…and I am happy for them.

But we are not one of them, we want to live our life differently…on the edge. Experiencing different things…suffering now to move to another dimension later…to get financial independence to be more free.

That’s where the excitement start.

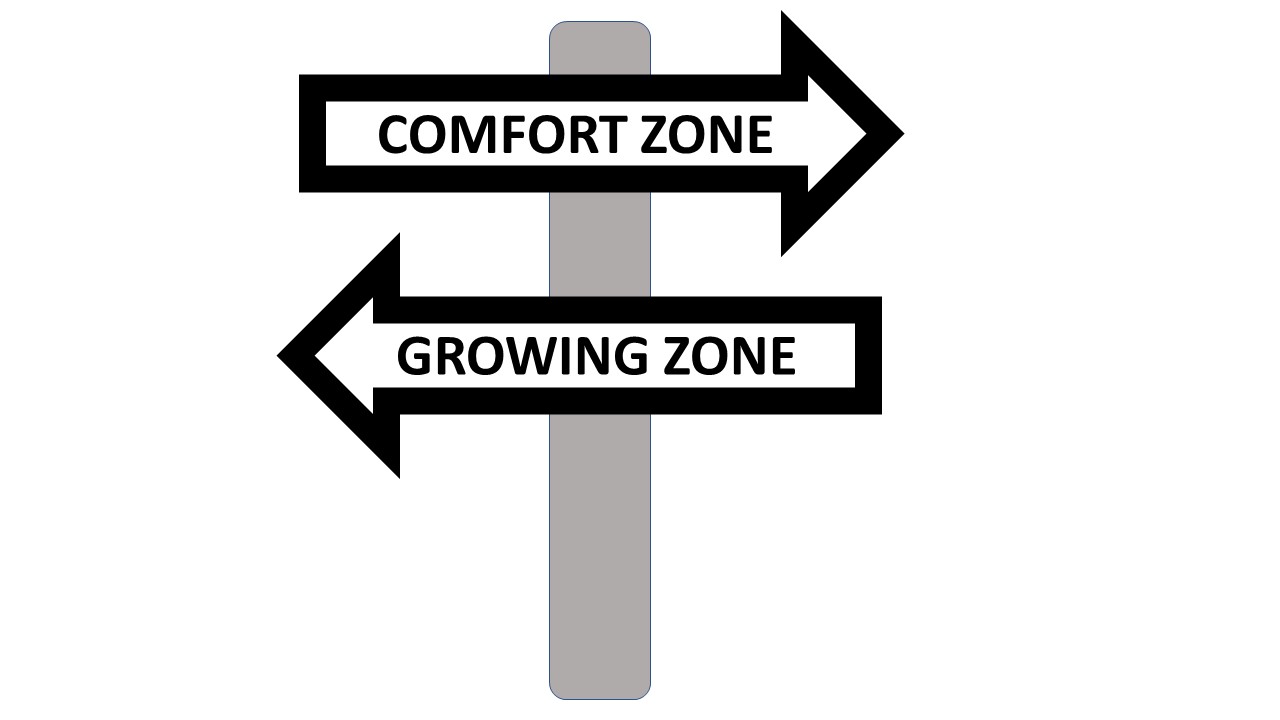

Living in a Comfort Zone.

Life is made of different comfort zones.

We go through them all our life.

When we reach a comfort zone it’s… well “comfortable”; the things around us are familiar, we know how things works, we have no fear.

When we stably reached a comfort zone and we are (again X2) too comfortable it’s sign we need to move to another one and not just adopt small changes in our lives (like Forbes suggests).

Because if you are too comfortable you are not growing.

Moving to the next comfort zone and growing is often painful…so we try to escape changes as adult.

A baby at some point will need to start walking.

He will fall and hurt himself (the pain) but the price is worth it…he will walk (the growth) because the curiosity is much bigger than the pain.

The same when we leave elementary school to middle school, the separation is painful, the environment is new but again we are growing!

And interesting enough in most of the cases (if not the totality) nobody regrets the change.

But later in life changing becomes more and more difficult because changes can be more drastic, not necessary needed and without a safety net.

Or very simply because as adults, we are more scared.

Typical examples are changing your job or leaving your home town; for someone it just seems impossible.

Leaving a secure job for starting a business, or the simple act of stop smoking.

When we decide not to change it’s in that precise moment that we stop growing, we stop speaking about the future; we speak only in present and past tense.

And we convince ourselves that we cannot do otherwise; “I would like doing that but… ”

The “Yeah but…” ; finding excuses to remain in the actual state.

How many times we had told ourselves: “I would do it but“:

I am too old I am too young I am too poor I am too sick My parents are too old or sick My wife has a good job My kids go to school and cannot change I don’t have time etc. etc.

Men need to grow, always, otherwise they must be dying.

The Turning Point

What trigger a change ; what is the revelation, the “Ah moment“, the turning point?

In every instant of our life we are the sum of all the experiences accumulated since we were born.

We think differently of what we were used to 10 years ago and will think in 10 year.

What we can understand now was unconceivable 10 years ago and in 10 years from now we will have a different understanding.

Someone call it wisdom.

I call it the turning point.

In my life different events triggered deep changes in my life and prospective; start living abroad, losing a parent, leaving difficult situations and people behind are some turning points of my life.

I start loving me more , taking more care about my self, saving money, believing I deserve more that I thought.

Hadn’t I never took critical steps (e.g. leaving certain situations or habits) my life would surely be on a different path, for sure worst.

It took courage to leave the comfort zone and luckily some events happened so fast and so concentrated to accelerate the processes.

But again I took the first step.

In our life we always know when it’s time to change; if we don’t it’s because we lie to ourselves (the “Yeah…but…“) or we created a thick layer around our micro world that make us blind.

I firmly believe our life should be on a path of continuous improvement; the changes can be small, microscopic (there is no need to leave your job or hometown if this is really what you love to do) but they must be there.

But then, why so many people are not happy around us? Why they complain about their job, misfortune, money, everything else?

Because they stop growing and being negative is the easiest path of accepting (or justifying ) their situation.

Every time someone complains with me about how unhappy is in a “changeable” situation (marriage, job, hometown) I candidly ask “Why don’t you change?” (and usually the answer is “Yeah…but“)

Every time someone asks me how I am doing my typically answer is “Great!” and I strongly mean it. Of course someday I am tired, sick and in a not perfect mood but it’s what inside of me that makes me feel great.

The feeling great comes from the love and passion to move ahead, to the next step.

I am falling and failing all the time and I will fall and fail some more.

Maybe I will not reach all my goals but some for sure and this is all that really matters to me.

Never Forget:

“We become what we think about, all day long” (Ralph Waldo Emerson).

If I love one aspect of the social media world is how it made clear that the priority of most of the people is to have friends (followers) rather than being a friend.

Let’s try with why:

The only think people want is recognition.

Very few people want to be a real friend… to establish sincere friendships in the online and offline world.

Thus there are billions of people thinking they have thousands of friends while nobody is friend of nobody.

Empathy is what can save the world, seriously.

We have to restart building our relationships, creating real time for real actions for real interactions.

We already talked about it no much more to discuss about it: stolen by the screen time.

2) Give honest appreciation to people.

Think deeply about people around you. think about their actions, how many good things they do at work, as parents, in the aspects of sports, arts , volunteering.

Don’t just give a fake like on their post in the social media.

People understand how fake you are.

Write instead a real message where you express your appreciation.

3) Be interested in what they do.

Stop being self centered.

Stop your arrogance.

Stop talking about you all day long.

The bad news?

People are not s interested in you.

People are interested in them…like you are interested in you.

Try to be instead sincerely interested in what other people do, in their interests, passion, love.

You will find a different and fantastic world.

The real world.

The world of people.

Of passions, stories, emotions.

And you will grow with it instead to remain your small me, confined in your micro world made of selfishness.

In the blogosphere there are 90%+ people absolutely self-centered, interested only that you read them and click on their ads, arrogantly thinking they, and only they, have something to tell you and you have to just listen because they think they are cool.

Be gentle and sincere.

Don’t be like them, you are better than them.

4) Stop complaining or criticizing.

The last think we want is someone popping in our lives telling us how badly we are doing our role of employee, son, father, friend etc.

Why so many people criticize then?

Because they think they are superior.

They want to control and humiliate other people to change them or just to validate their points of view because they feel insecure.

Great mistake.

Be humble instead, never criticize, even thought you might have a valid point during an argument with somebody.

5) Listen.

People don’t listen and if they do without empathy.

I don’t.

Very likely you don’t neither.

We are too busy to think exclusively about ourselves that we don’t simply care about what other people have to say.

Simply because we don’t care about people.

Nobody don’t care about anybody.

And this behavior got worst and worst with the advent of the screen.

Before kids were playing in the streets and in the fields.

They were climbing the trees and creating real relationships and friendship scratching their knees playing football or soccer.

Today the only thing they do is playing on their phones.

You see them sitting, without talking, immersed in their screens, isolated from everything.’

They don’t care to have friends.

All they want is the pixels on the screens.

They have no interest to listen to you, they have no interested to listen to anybody.

Stop this craziness right now

Put the phone down and start talking and listening to the hearth of other people.

They will do the same with you

Rebuild relationships.

That’s what you need, not another fake like on an horrible picture you posted on your social

Nobody cares about it. In the same way you didn’t care about the last like you gave to somebody.

Let’s get all real, the world need us, right now.

Be a linchpin not a cog. (thanks Seth)

It’s imperative to limit the screen time to children who are several times more vulnerable to the devastating effect of screen time on the brain and on the body.

Especially for preteen and teenagers the brain goes through major changes and the impacts of the screen is devastating on attention disorders (if you have a kid you can experience it everyday), emotions and personality, creativity, self-confidence, learning and social skills and sports.

In 2010, researchers found that kids who logged more than two hours a day in front of a computer or TV screens had a higher chance of psychological difficulties on a standard questionnaire.

4. Highly addictive

Do you notice how addict you are on checking continuously your phone, email, wearable etc.?

It’s call addiction.

Every year trillions of dollars are invested in R&D of screen makers to keep you glued on their device.

User Experience is called, I call it addiction.. and a nasty one.

5. Pathetic: Losing human relations

There are no restaurants where I don’t see pathetic couple or group of friends not talking and just glued to their phone.

That’s sad…and as said pathetic.

6. Dangerous

Text and drive anyone?

Or text and walking…(now forbidden in some countries finally!)

https://youtu.be/_cznepJAbyg

7. Stupid

We spend hours doing stupid and useless stuff on the phone, not looking for the cure of cancer.

We need to stop and right now.

How to reduce the screen time

Decide right now the screen time that is absolutely essential.

In my opinion that’s teh max you should allocate:

Facebook: 5 minutes

Twitter: 5 minutes

LinkedIn: 10 minutes

Instagram: 5 minutes

Personal E-mail: 10 minutes

Mindless Browsing: 5 Minutes

News Reading: 10 Minutes

Financial, Economy: 15 Minutes

Blogging (amateur…otherwise is considering job): 20 minutes

Others (Redditt, Pinterest etc.): 15 minutes

Total: 1h – 40m per day.

This should be your max screen time per day.

Be very clear on when you will use your screen time (e.g. Instagram only immediately after dinner or never) and STICK to the plan.

Here we are…2019…it really seems yesterday when 2018 started…

Exactly…time goes by too fast…and too fast we committed goals only to faster forget them…

Every year is getting shorter never seem to find the time. Plans that either come to naught or half a page of scribbled lines Hanging on in quiet desperation is the English way The time is gone, the song ishttps://youtu.be/JwYX52BP2Sk over, Thought I’d something more to say.

Many of Financial Independence Blogs rotate around a dogma:

The 4 percent rule.

Simply said and based on a study called the Trinity Study:

if you have a certain amount of money invested in a mix of stocks and bonds, 4% is roughly the maximum rate at which you can withdraw from the principal and being sure you will not run out of money.

Based on that dogma here another truth derives:

If you have saved 25 times of your annual spending …

Congratulations!

You reached Financial Independence.

(so hurry to give your boss your 2 weeks and your a well deserved Margarita right now!)

Why this dogma does not work

Life happens (and this is expensive)

The 4% is the max withdrawal rate…and perfectly matching your spending.

What about if you need to spend more?

Exactly.

2. Living in America!!!!

Most of the blogs talking about Financial Independence and Early Retirement are (curiously) based in one of the most unfriendly Countries for Retires: the USA.

Plainly said:

USA is one of the greatest place to make money while you are young, healthy and employed.

USA is also one of the greatest place to spend ALL YOUR money if you are not young, healthy or employed.

If you are sick and not insured (or under insured) in the USA you can easily spend thousands of dollars to treat a small health issue or all your capital…

The Trinity study and others of its kind have been sharply criticized, e.g. by Scott et al. (2008),[5] not on their data or conclusions, but on what they see as an irrational and economically inefficient withdrawal strategy: “This rule and its variants finance a constant, non-volatile spending plan using a risky, volatile investment strategy. As a result, retirees accumulate unspent surpluses when markets outperform and face spending shortfalls when markets underperform.” Laurence Kotlikoff, advocate of the consumption smoothing theory of retirement planning, is even less kind to the 4% rule, saying that it “has no connection to economics…. economic theory says you need to adjust your spending based on the portfolio of assets you’re holding. If you invest aggressively, you need to spend defensively. Notice that the 4 percent rule has no connection to the other rule—to target 85 percent of your preretirement income. The whole thing is made up out of the blue.”[6]

I become nervous…

Four percent might work…or maybe not…

Whatever…

Now what?

My rule of the thumb is pretty simply.

Align the percentage with the net return of dividend from Index Fund (as of today below 2%).

Why?

Because it is safe.

Because no matter what my capital is untouched and I have a good margin.

I am not an economist.

For the same reason why we all should invest in something more predictable with index funds tracking the total market and not try to invest in single stocks, we need to play with our money and life with a very ample margin.

Think with your head.

Be safe, even if this means retire few years later.

No, you don’t need that iron and plastic box sitting in your garage or parked (maybe far) somewhere in the street for seven reasons. I am going to show you 7 reasons why you don’t need a car…and if you really need it how to spend 10 times less than today.

Let’s turn on the engine.

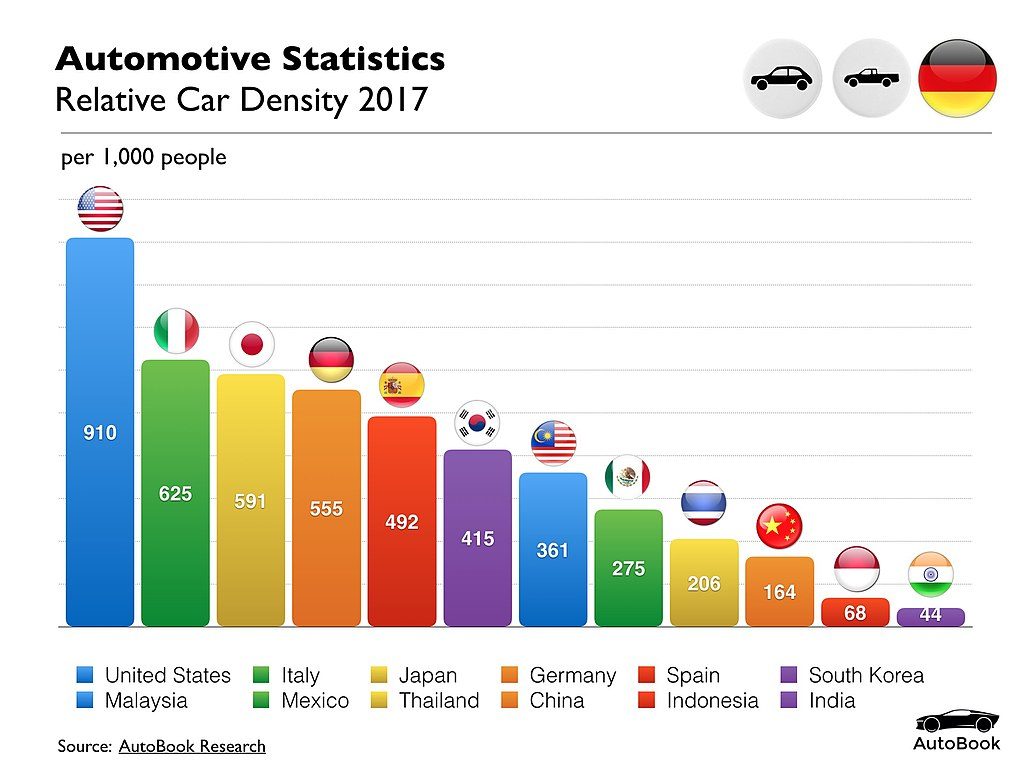

Purchasing Cost

The Country with Highest Car density is USA (are you surprised?) with 910 cars every 1000 people. In second place there is Italy with a density of 625.

Highest Car Density in the USA…how surprisingly!

On average the cost of a car in the USA in 2018 is roughly $35,000 (there is a nice post of Financial Samurai on the cost of cars in the USA you can find here) .

Expensive…isn’t it? Let’s go deeper….expensive vs what?

How much a family is making in the USA, Italy or Spain per year?

Americans makes roughly $60,000 per year (before taxes…let’s say $45,000 after taxes) and (on average) spend $35,000 for a new car. Keep in mind these figures are averages…but they give a clear indications on the impact of owning a car.

Country

Average Car Cost

Average Salary after Tax

Car Cost vs Annual Net Salary

USA

$35,000

$45,000

78%

Italy

$24,000

$21,600

111%

The impact is devastating: Americans spend on average three quarters of their annual salaries on purchasing a car. For Italians one year of salary is not enough…!

In 2017 only in the U.S. more than 40,000 people died in car accidents, 110 every day! Car is one of the most dangerous place to be and full autonomous driving (i.e. no more human driving cars) is still decades away. People are scared of planes and lightening while they face dangers thousand of times bigger daily.

Health

On average Americans Spend an Average of 17,600 Minutes Driving Each Year…that is 293 hours. Almost one hour everyday… Add thisto the 8-10h sitting in the office and you have a more complete picture. Also consider that the posture and vibrations during driving have much worst effect compare to the office sitting

Pollution

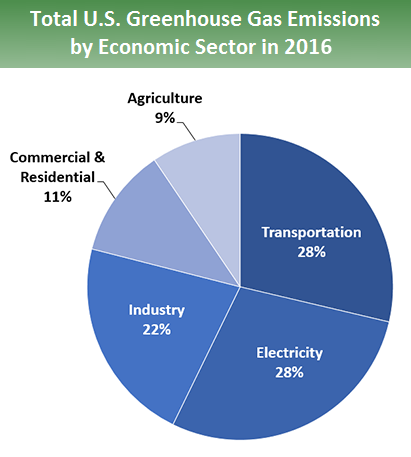

According to United States Environmental Protection Agency Transportation?, the transportation sector generates the largest share (nearly 28.5 percent in 2016) of greenhouse gas emissions. Greenhouse gas emissions from transportation primarily come from burning fossil fuel for our cars, trucks, ships, trains, and planes. Over 90 percent of the fuel used for transportation is petroleum based, which includes gasoline and diesel.

Impressive. Isn’t?

Additionally the dependence of fossil fuel created the (often negative) political dependence on the Country producing it. But you already know it…right?

You Simply don’t use it

How long do you think you use your car? 30% of the time? 20%?

What about 4%?

An interesting report found out that in Britain the average car is parked at home for 80% of the time, parked elsewhere for 16% of the time and is only on the move for 4% of the time.

4%…think about it…you spend tons of money for something you use only 4%.

Conclusions

Owning a car is one of the main negative think fro your finalce, heath and sanity. If you can’t really give up the metal box consider these alternatives:

Buy a use one: purchasing a second hand car can drop the cost of your car up to 40%, especially if you can find good quality used car (like in the USA)

Keep the car longer: don’t fall in the lures of owning the latest brand new car…for one hour pleasure you will have years of regrets. Buy a decent quality second hand car and keep it at least 10 years (yes I said 10…modern car can last in pretty good conditions more than 20 years)

Analyze the Alternatives Unless you live in a very remote area there are many alternatives to car: public transportations, biking, Uber (even thought for Uber the Risks of accidents are still there), walking!

You decide to buy and use a car. Acknowledge that…and avoid it if you can…

How can we possible follow everything?

We cannot…even thought we pretend.

The same happens to everyone, too much (addictive) inputs and not enough time.

Thus the question to all of us bloggers.

Who’s reading us?

The blogger dilemma

Who is really reading my blogs?

Who’s reading it with involvement (or only to use my audience to his advantage)?

Should I keep writing if nobody is reading me?

Am I bringing value? ..or better… Do I care to bring value to the community or I care only for myself?

Grabbing the attention of people in internet is increasingly difficult due the one (even less) second attention span we have today in these era of overflow data. We get attention when we touch some nerves, when we say something interesting, useful, when we are able to present it correctly.

A fantastic picture exploding on the screen and our face, a blog post addressing exactly the topic we think about all day long, a video that makes us cry…

In a nutshell…when you deliver emotions:

Do you have something to say?

What is your message?

Why should I be here reading you and not the other millions of blog out there or playing Candy Crush?

Where is the VALUE FOR ME in what you say?

Where are the EMOTIONS?

Will I be a better person after reading what you say?

Few years ago (20 I would say) we were barely able to keep contacts using landline phones and only with people whom we knew.

With the advent of the cellphones we extend our reachability everywhere and all the time.

Even thought you might be used to this reality or you are too young to remember the world without cell phones, think for a moment on the great impact of it on our lives.

Think about the implications of being able to reach an audience of 3.2 millions people right now.

Well…I am doing it…right now…with this post…and you are one of those 3.2 millions people.

I don’t know who you are.

You don’t know me (at least personally).

But we are connecting.

You can change my life right now just sending me an email, a tweet or a comment.

I might have already changed your life.

Blogging and money

Who is writing a blog has a passion, whatever is the message.

The passion is usually so strong that the blogger would love to blog all the time thus (unless the blogger is very rich), he would love to make blogging his primary source of income.

All considered, if someone wishes to make some money from blogging, this desire is not only fair but sacrosanct because if I, blogger, am producing and offering value (thus I have readers) such value should be rewarded.

Conversely if I don’t produce any value…very likely I will not have readers thus I will not make any money through ads or products.

That’s simply and brutally the real law of the market

No value produced = no money gained

Why should it be the opposite?

The problem is that most of the people employed (so a big portion) cannot realize the equation value = money because they cannot link the value of staring a computer in a cubicle with the making of “something” (a products, a line of code etc.).

Even worst, sometimes (often?) in the corporate world such link doesn’t even exist…people doesn’t produce any value but they get the paycheck anyway…overachievers will compensate their lack (and get frustrated).

Conversely, blogging is pure entrepreneurship: you get money in direct proportion of the value offered…no office politics, cheating or friends of friends game is playing here.

Always remember the 4P of marketing, they apply also to your blog:

P as your Product: the Value of you offer

P as your Promotion: are you promoting your blog in every social channels? Are you networking with other like-minded blogger?

P as Place: Is it easy for the reader to access your blog posts?

P as Price: Are you offering a service with a reasonable price? Are you offering it for free? Or it’s too expensive?

Understand that if only one P is not satisfied by your offering, your blog will be a major failure.

Your product has no value? Nobody will buy it (in case of a blog, nobody will read it…why wasting time to read things that have no value for the reader)?

Your blog is great but you don’t advertise it enough? Nobody will find it.

Similarly if you publish it in a difficult website to navigate or in Social Channel nobody uses, people will have trouble to access it.

Your e-book or course is great but you charge too much vs the perceived value of the reader?

Nobody will buy it.

Conversely, you are not charging anything for your products or use affiliate links? You will not have revenues (in same cases this is acceptable since not everyone is blogging for revenues).

What to sell

Making some money on the blog can be fairly immediate and easy with affiliate links and random ads. One of the rule of the thumb (you can find many rules on the web) is that you make roughly $1/year for each visitor you have per day with a Bounce Rate of 100% and roughly 1000 pages published on your blog using Google AdSense (with a CTR of 1% and CPC of $0.25).

Without going into the details…yes you can make some money from your blog inducing your readers to click on Ads but you need a lot of traffic so something to say (again: No value produced = no money gained).While I do believe in the power of marketing and creating a network of bloggers/people with identical interests I am a firmly believer that readers sticks with you if you have something valuable to say.

Why I don’t believe in Google AdsYou might have noticed I don’t have Google Ads on this blog (and in others blog).

Conversely I had them in others websites used for pure marketing/commercial activities where they makes sense since the only goal was promotion of products and services.

Blogging for me it’s a different story, I do want to share with you my story, suggesting you some products I use and consume and I really want to share to the world since EXCELLENT for me and making some money in the process.

Filling my website pages with Random computer generated Google Ads suggesting you some Shrimp Antonia Bag Pink Size One it is simply not for me.

Conversely suggesting you to use great tools like Personal Capital to keep tracking your finances is something I really believe into it like in other products I do really use and enjoy on a regular basis.

What now?

Use the gift of communication to be brilliant, to express yourself, to change the world.

Don’t scam people or treat them like stupid, take out those annoying Google Ads pushing your readers to buy crap just for you to get the commissions.

Have something to say, bring value in this world and value will pay you back in form of money, notoriety, personal satisfaction or just inner peace….the most important one.

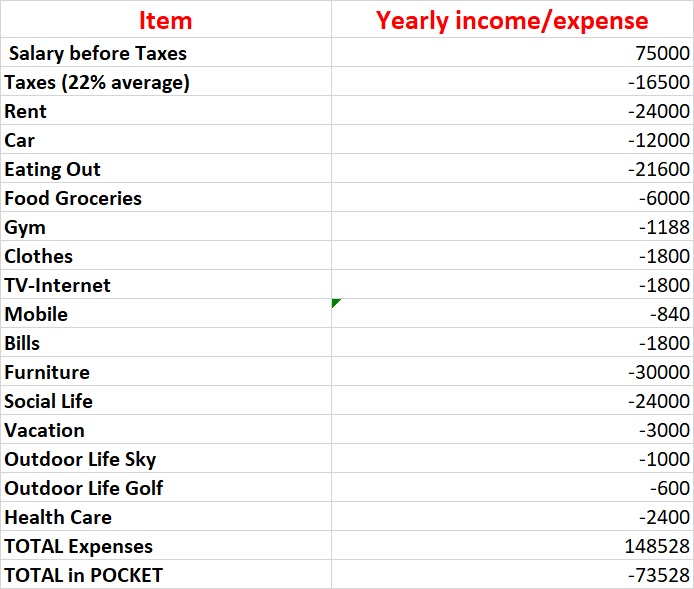

Joe was lucky…his parents paid for his college in a middle end university and for his used car (now ten years old).

John is very happy with his salary…a lot of money…

HR mentioned him about something called 401K and the importance of contribute to it…the company match..and the fact he is supposed not to touch it before 60 years….

Naaaahh this 401K is really complicated and looks useless and risky…then touching the money only when I will be 60 years old and very likely dead…? No Way!

So Joe starts his single life…

House $2,000/mo

Mhhh…the new apartments downtown Denver look very nice…$2,000 maybe a little expensive but…hey they are walking distance from all the cool bar an d restaurants of the area and you know I don’t want to move to a single family in the suburbs..I will do when I will be 40 years old and with two kids!

Bills (Electricity, Gas, Water, Misc) $150/mo

Joe is seldom at home, but when he’s there he wants to forget how cold is Colorado…!!! Luckily apart of electric bills he doesn’t spend much more on other utilities.

Car $1,000/mo

The 2015 Nissan look very old and crappy. I cannot leave in this suburb with this car and go out for a date with it…

Since now Joe is working credit is easy…so…what’s best than buying a new car especially now that there is a fantastic offer in the BWM dealer?

Put some gas, parking and Insurance…roughly $1,000/mo…no bad right?

Eating out $1,800/mo

Joe never cooked at home and his parents never thought him.

Anyhow there are so many restaurants downstairs for a quick dinner, Starbucks for breakfast and a great selection of salad bars around the office for a healthy lunch!

12$ Breakfast 18$ Lunch 30$ Dinner…not so bad!

Food Groceries $500/mo

Joe has no time and he doesn’t cook so he doesn’t need much food.

The upscale groceries store is just walking distance from his apartment

and hey..so many organic products!!!

500$/mo in so healthy products (too bad so many are thrown away because Joe is too busy and he forgets the expiration date)

Gym $99/mo

Mhhhh all that food and 8 hours sitting in front of the computer is manifesting big time on Joe belly…time to Gym..!

There is a cool Gym downtown…the price…a steal…all you can go open 24h and with swimming pool only $99/mo…!

TV – Internet $150/mo

When Joe come back he needs some relax..so what better than a 80″ 4K TV (5000K$) with a nice Internet + TV Cable + Netflix package for only $150/mo?

Mobile $70/mo

Joe has many friends right? So the unlimited data package at $70/mo is a must for his video call and social network…hey there are more expensive one…you know?

Furniture $30,000 (one time)

Having lived with his parents Joe doesn’t own practically anything…

and he has a 1200 square feet to fill now..!

Surely he doesn’t want cheap IKEA furniture in his posh apartment…besides he just discovered that in Boulder downtown there is a cool and trendy furniture store that import directly from Italy.

Wow…he has practically to buy everything…total expense $30,000…but it’s one in a lifetime!

Social Live $2,000/mo

Denver it’s so cool….! He cannot resist his clubbing, bar hopping and restaurant before Thursday (sometimes even on Wednesday)…

$500/week…well spent!

Clothes $150/mo

I really cannot go to work and in the club with the Ninja T-shirt I was using in the college…I need to dress like a young professional man now…Time to invest in my look!

Vacation $250/mo

Being a software engineer at XWZ tech Inc is very stressing!

Joe really needs to take a break from the cold of Colorado during his weeks off.. what’s better than hopping on a plane to Mexico or Hawaii…? $3000 really well spent!

Outdoor life Sky $1000 (one time)

Joe live in Colorado…he must learn how to sky…!

And so many people in the office go….

Here he’s with a brand new unlimited seasonal pass for only $999 (it was $1200…what a deal!)

Outdoor life Golf $50/mo

Well…with so many sunny days, great golf courses and many Managers and Directors playing in the company Joe must play golf during summer…poor Joe…with all the hours spent in the cubicle he really needs some fresh air

Health Care/Insurance $200/mo

Joe’s workplace offers a great Health Care package with only $150/mo from Joe pockets. Add a couple of visits for cold and small stuff (Joe is so young!) and the total cost is very limited.

The first year is gone…what a year!

Let’s crunch some numbers

Ok…it was just the first year!

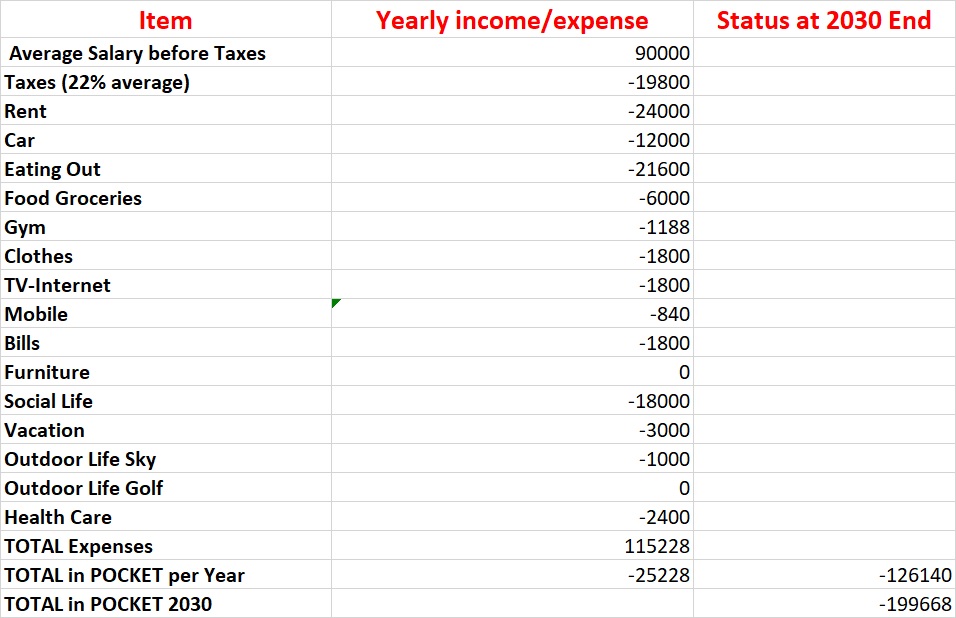

2025-2030

Joe had great 5 years as single guy in Denver.

The job was doing great…now he finally reached the six-figure milestone!

He also found a nice girlfriend and got engaged…thus the sweet single life is getting to an end soon.

Expenses wise he’s still doing the same life…just cutting off golf (too boring) and social life since he found a stable partner.

The good news is that Joe parents gave Joe (only child) their second home and he sold it for $250K thus so far no need of credit card debts.

Life is great for Joe!

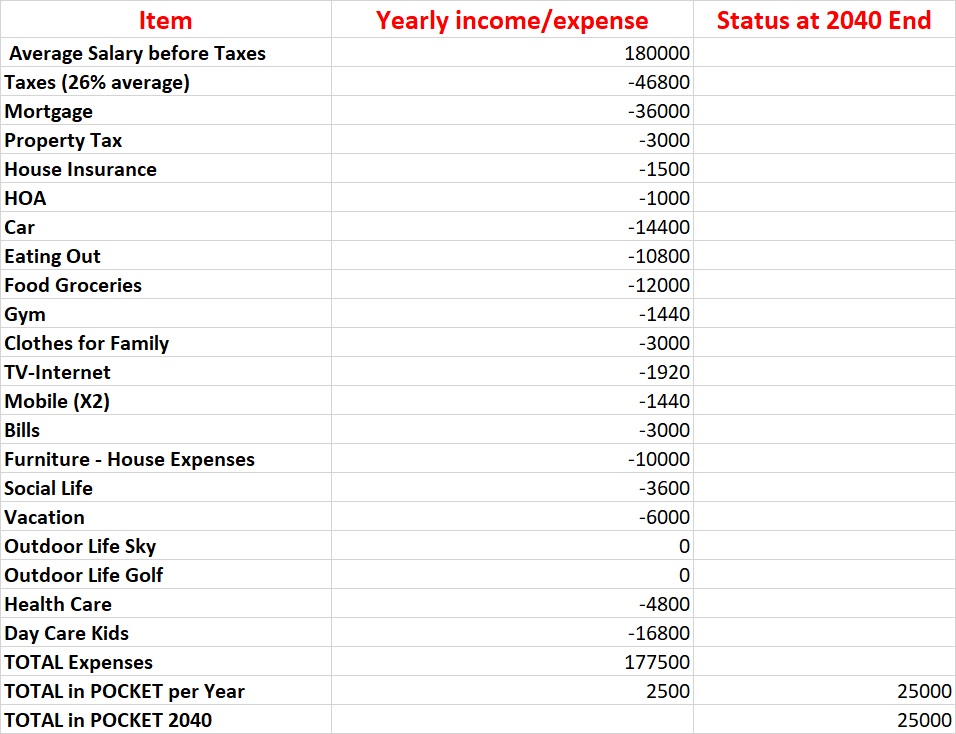

2030-2040

Joe gets married and two kids enlighten his family life!

Joe also get promoted as Director of Engineering in a new high-tech company close to Boulder and his salary and benefits dramatically increased.

Also the health care expenses increased with two kids in the family.

Kids also added day care expenses to the balance even though Joe’s wife is not working.

And of course a bigger family requires…a bigger house and cars ! (and vacation budget).

Luckily the social life expenses almost dropped to zero….

Here we are…

Some money saved at 40 years old…

Here it is Joe at 40 years old with some money in his bank….almost $25K…!

Joe feels almost rich with that amount available…now he can afford that vacation in Europe with the new 100″ TV or why not a boat or a new car.

$25K are a lot of money…isn’t ? Especially when almost of his peers are into deep debts…!

Of course Joe doesn’t want to hear about investing…he knows people talk a lot about Dow Jones, S&P, mutual funds…too complicated and surely a scam.

In any case Joe already made a great investment with the house…is not real estate the best investment around?

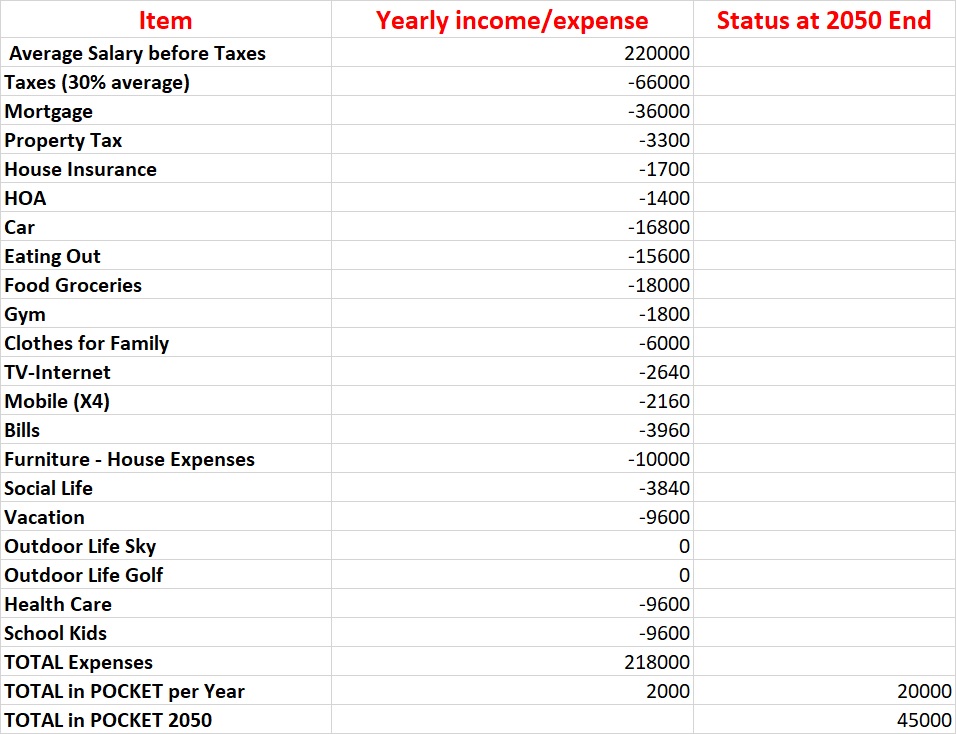

2040-2050

Kids are growing.. both are in High School now.

Joe got another promotion as Vice President of Engineer in a start up….those are the peak years of making money.

Savings are Increasing!

He’s happy because when he turns 50 years old he reaches 45K$ in saving (all of them in his checking account since he’s still not trusting the traps of investing!)

Also all expenses increased: Food (two big boys are always hungry!), Health care, Mortgage, Property Tax, Car Payments, Bills, Clothes etc but likely Joe is making great money…so no problems!

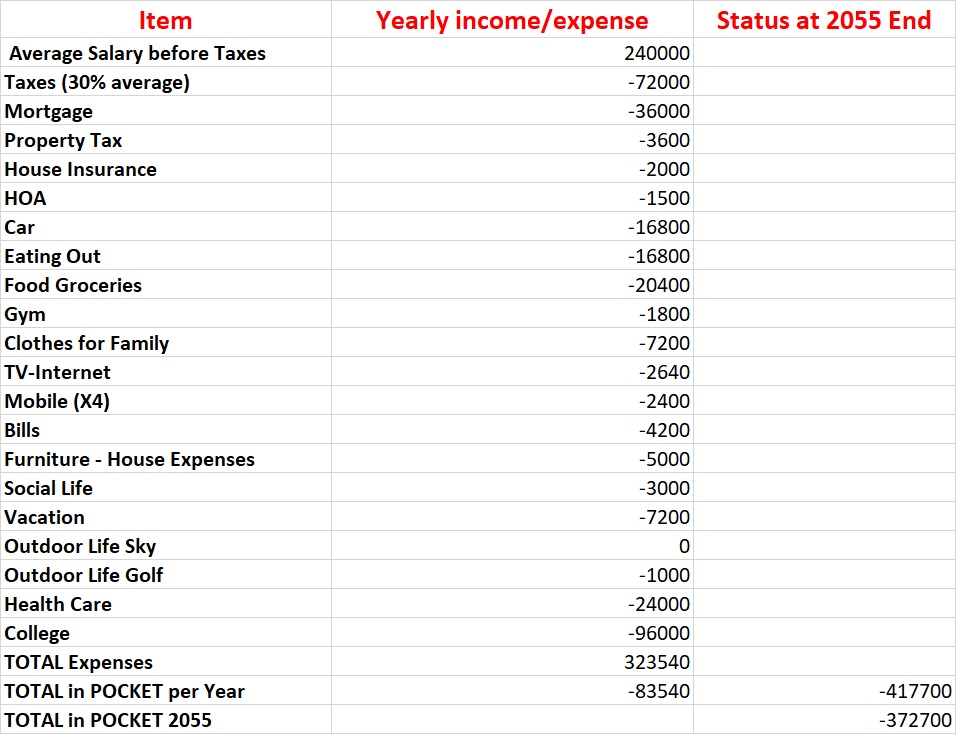

2050-2055

College years for the kids…both in an affordable one so the expenses are limited to $4K/mo per kid…all included (no bad right?).

Health care expenses are going up…Joe and his wife are both in their 50 and co-payments and dentists expenses increased and the kids are still on their insurances plan.

Joe started again with golf thinking about retirement…

Economically the situation started deteriorating…not only Joe spent all the saving but now he has almost $400K debts at 7% average in college loans and on a couple of credit card.

College years…

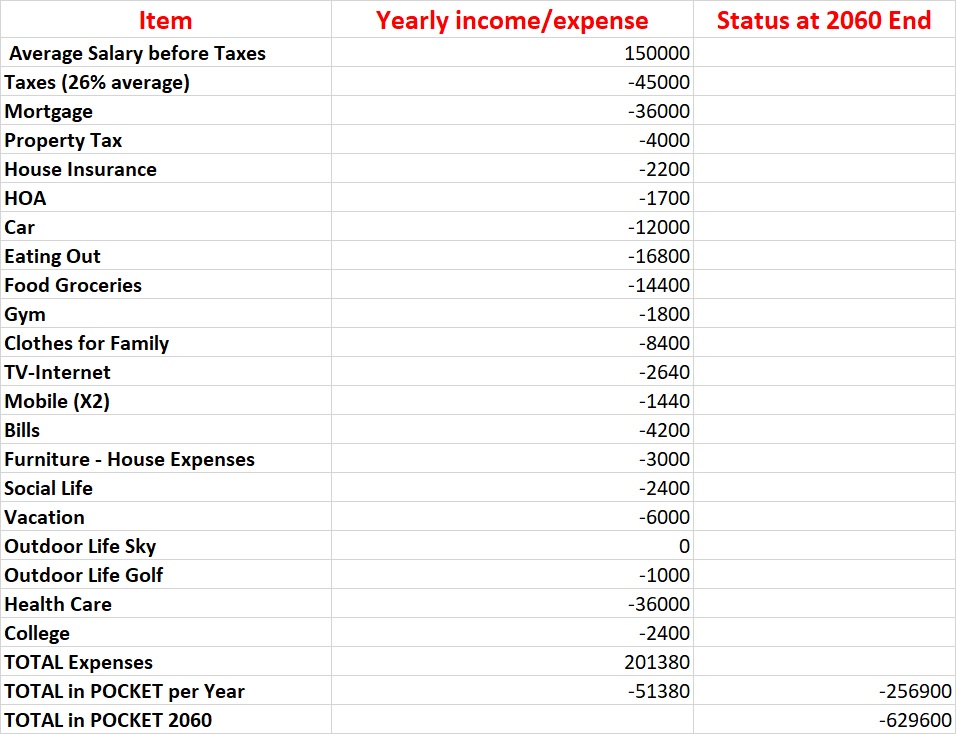

2055-2060

Joe and wife don’t think downsizing from a big house (now empty since the kids left) and luxurious European care is a wise move.

After all they are affluent middle class right?

Joe was caught in a sudden layoff due to economical crisis and, as usual, the highest paid are the first to go.

He stay almost one year out of workforce and he found a job as Manager R&D with a substantial pay cut.

Luckily the kids are practically out of college and all almost all the expenses of Health care are for him and his wife.

Unfortunately their expensive lifestyle is costing more than Joe salary…roughly $50K are going into credit card debts per year to compensate the expenses.

It will go better now with kids out of college!

Debts are increasing

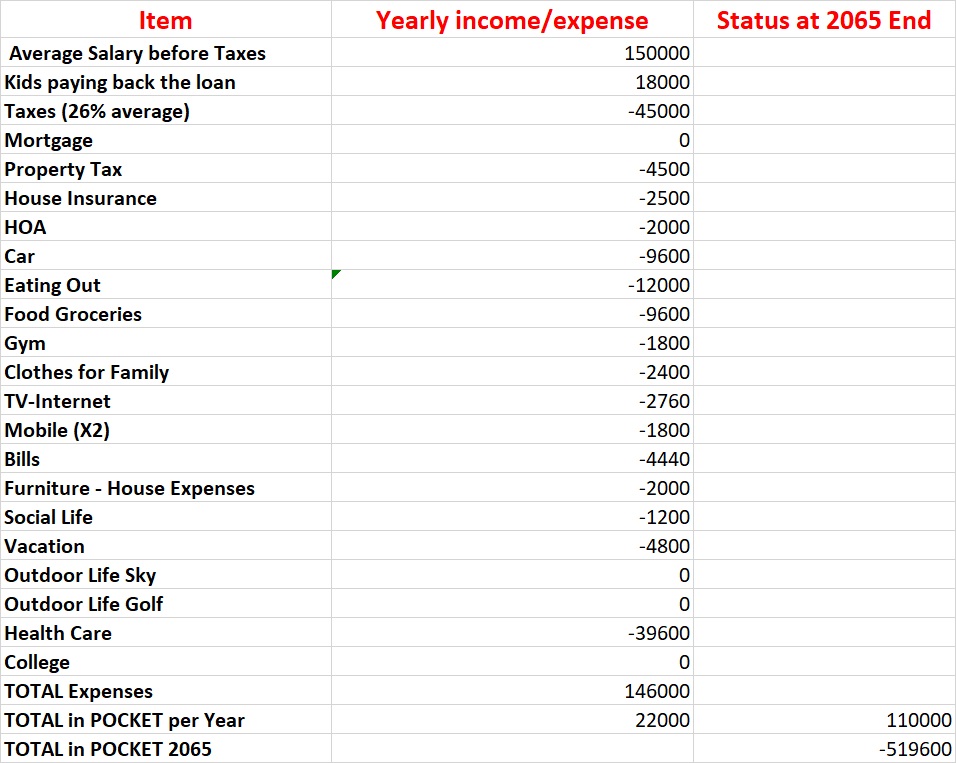

2060-2065

Joe job is stable and kids finally are paying some of the college loan back.

Great news…no more mortgage and Joe finally decided to buy a slightly less expensive car.

All the other expenses are going down as well apart the health care since they both went under a couple of surgeries and therapies.

They were able to save more than $100K in five years…not enough to finish to pay the debts…

Some savings are back…

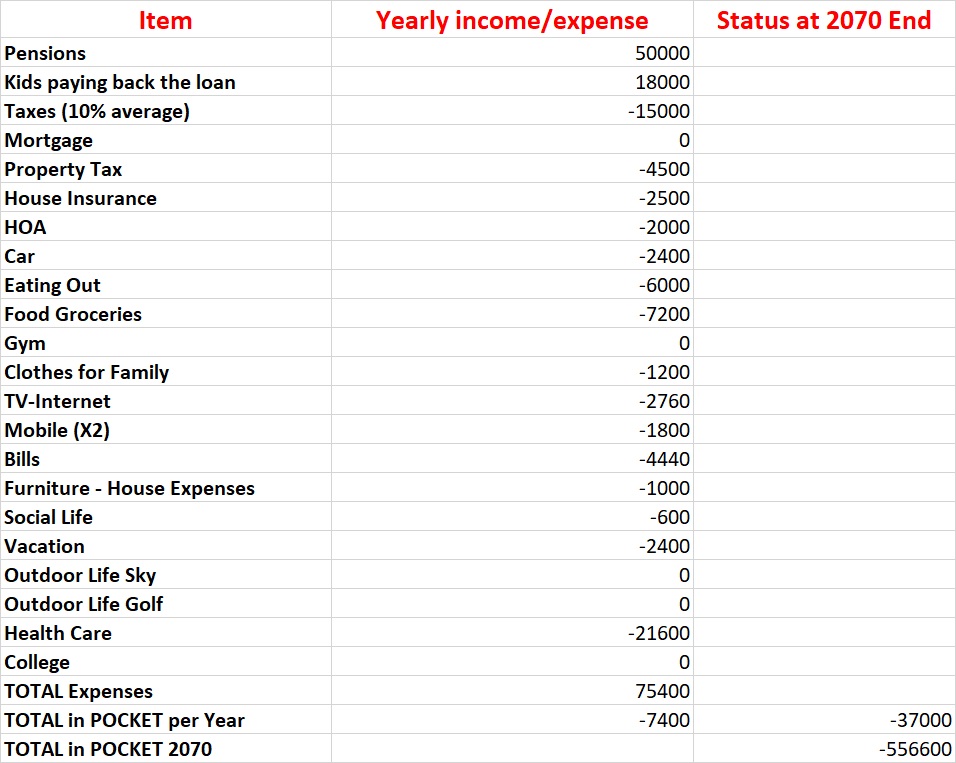

2065-2070

Joe retired.

Between Social Security and Companies pensions is bringing home $50K before taxes.

As we know Joe never believed in investing or 401K so the $50K before taxes is all they have.

Kids kept giving the money back for the students loans but in 2070 they repaid everything and now they have their own family to take care of.

Joe and wife are roughly more than half million dollars in debts.

The retirement

2070… and the future

So what now…?

Joe and his wife now are forced to downsize the house and giving up the expensive cars.

Doing so they are able to reduce their debt to $300K in 2072.

Too big anyhow the debt (at 12.5% interest on 5 different credit cards and one home equity) to be repaid.

Joe and wife will likely die poor in some hospice giving as gift the debts to the kids.

This is no fantasy

Every year thousands of people end up like Joe and his wife; despite making a great salary while young and having his parents paying his college.

Every years people cannot realize they are spending more than what they make and that they need to save money for the future.

This is no fantasy…this is the sad typical middle class life.

Ok…let’s start with the definition (thanks Wikipedia)

…that retailers traditionally operated at a financial loss for most of the year (January through November) and made their profit during the holiday season, beginning on the day after Thanksgiving.[7] When this was recorded in the financial records, once-common accounting practices would use red ink to show negative amounts and black ink to show positive amounts. Black Friday, under this theory, is the beginning of the period when retailers would no longer be “in the red”, instead taking in the year’s profits…

So…what’s the link of Black Friday with big sales and the push you to spend…?

Nothing.

Just another day created to make you waste your hard-earned money (like Christmas, Valentine day, Mother’s day, Father’s day, Teacher’s day, Your Neighbor day (last one I made it up but I am pretty sure they will invent it soon).

The word today is:

RESIST RESIST RESIST!

Yes…like him

Why? 5 Reasons…

1 You save 20% to spend 30% more

Black Friday is a big, fat bait.

Attracted by the 90% off Laptop (that most of the time gets sold in 5 minutes) you enter in the store (online or offline) and…voila…you exited with ten objects that you absolutely didn’t need it but you bought them just because they were 40% off…! (tell me the truth…how many memory cards or disk dusting in your drawer do you have…?).

2 You can find better deals

Make an experiment…just check the price of a product during the Black Friday Sale…the regular price when it’s not on sale and track the price during following 6-8 months after Black Friday.

You will be surprised…

If you don’t want to wait just read this study from NerdWallet:

In a NerdWallet analysis of 27 Black Friday advertisements, 25 retailers listed at least one product for the exact same price in 2014 as in their 2013 Black Friday ad. That means 93% of retailers are repeating Black Friday products—and prices—from year to year.

Surprised, right?

3 You are going to buy old stuff

Yes..yes…the brand new TV is 80% off but very likely they have only 2 in stock!

The rest of the items are older items (usually the previous year) that will be on sale anyway.

You will end up buying this one…

4 Black Friday Day last more than one month

Already in the end of October we start seeing the Black Friday month deals…then the Black Friday day deals… then the Black Friday day deals…then the Cyber Monday deals…then…the Christmas period sale…then the New Year day sale…

If everything is always on sale every time…where is the deal?

I personally love my job…with 20$M I might decide to do it for free (or almost) part-time and as freelance (thus removing any kind of obligations).

Conversely if you would run away from your job only due to the money you are in trouble.

Working represents 60% (even more) of your waking time and 90% of your thinking time.

8 hours sleeping – 9 hours working – 1-2 hours getting ready and commuting to/from your job

What’s left? 5-6 hours where you will likely relax from the stress of your job?

It makes no sense.

Especially in these years where the opportunities of picking up a job that might excite you abundant thanks to internet or the globalization.

So what? Put the work on it…

You might be a digital nomad, move to another country to cover a position where your skills or knowledge of the market are needed (think about USA or European companies with branches in Asia for examples), be a blogger, going in the digital music, video industry and other tons of jobs.

The stereotype of 9-5 until 65 white collar in a office is not the mainstream anymore and less and less for the blue collar as well.

You can pick a job that you really love, more than ever.

But (and this is a huge BUT) you must put the work into it.

You must be obsessed by it.

You must think bigger than having as unique goals to buy a house and a car ten times more expensive than what you really need just to keep up with the Joneses.

Waking up in the morning ready to jump from the bed just to do it.

Otherwise winning those 20M$ is the only option and let me tell you that the chances are pretty slim.

Could you be loved?

Could you be loved?