Maybe some of you have heard about Vilfredo Pareto or the 80%-20% law.

Mr. Pareto in the beginning of the 20th century observed that roughly 80% of the land in Italy was owned by 20% of the people and that a similar proportion was valid for the other countries. As of today this unequal distribution is more and more valid (some studies show that 40% of total asset in the world are owned by 1% of population).

The same law applies in business; usually 80% of revenues of a firm come from 20% of the customer.

How does it apply to our life?

Think about the results (positive or negative) you got from your life (personal, business).

Can you see the correlation?

Every day, every morning, focus on the 20% causes that produce 80% of your results; put more attention on the positive 20% and eliminate the negative 20%.

In my case I noticed that keeping an open mind and networking actively and sincerely (really caring about people and co-workers) made me found very good job opportunities (other people offered it to me, I didn’t even need to searching it) that I would never found just sending resumes around (80% of efforts!)

Me after the job offer

On the negative side: exercising and kicking 1-2 small bad habits produced a great benefits on my health. Moreover; complaining (How to stop Complaining for good in 9 days) creates more than 80% of the troubles and limitations in our life.

Eliminate it right now!

We need to deeply understand what is really important on our life and focus on it. This would mean to cut some activities at work (some people will complain but stick with the principle) or sacrifices (cutting TV is an ideal!).

But I can assure the results will be astonishing.

Wake up with a crystal clear picture of what it really matters and work on it; eliminate the inessential and reach your goals, the one that really matters.

First Things are the most important things for your life; the only ones that really matter.

Typically First Things are:

Exercising

Actions to reach personal goals (whatever they are)

Saving and Investing Money

Spending quality time with your family

Educate yourself

Finish (excellently) all the tasks at your job (if you have one)

That’s it…nothing more…nothing less.

The rest is only noise.

Instead….

How many times did you schedule to exercise (How to avoid to die young) after work and inevitably skipped ?

Work is an insatiable animal, it devours our time; the last call or email typically takes 2 hours and we end up leaving the office at 8.00pm. So long exercising or read that book that sits on our night table for 1 year!

What you need to realize is that everyone wants our time and moneyand most of the time exclusively for their benefit.

Saving money is the same (The 3 simple habits to Reach Financial Freedom) ; if you wait the end of the month saying “I will save what I will not spend this month” very likely you will end up saving a lot less (if zero) than if you had immediately (after you got your paycheck) transferred some money to a saving account.

You and me know right…?

Instead….

You need action, focus and discipline

If you start our day scheduling the “First Things” we will be sure to move on in life.

Don’t do like this guy…(yes I love him…)

This means waking up before everyone else and setting up 2-3 hours to complete the tasks.

Reading or writing that book (or blog) or concentrate on your next business with kids, wife or peers around it’s impossible; you need to find a timeframe for yourself alone.

Yourself alone.

Not everyone is a morning person, I also experimented working late a night (when everyone was sleeping) , however I reached the conclusion is better to complete the “Thirst Things” in the morning.

Typically (unless you are very determined) it’s difficult to always leave work at 6.00pm to go to the gym, or schedule to work from 10pm to midnight.

Your job, peers, kids or wife will put a lot of pressure to get also that timeframe.

Early in the morning there is no that risk; you will have 2-3 hours for yourself.

I understand this translates in waking up before 600am (I wake up at 530am shooting for 8 hours sleep) but it’s a sacrifice to get your life back from the madness of the day, where everyone wants a piece of you, often for not important (at least for you) issues.

They must be the most important two hours of your life, necessary to refocus, giving a direction to your life.

You must see these 2-3 h as the timeframe allocated to stretch your comfort zone (The most dangerous place to be!); the rest of day must be dedicated to enjoy the, this time, valuable comfort zone you created (with kids, wife, in the hopefully nice place you created).

Roughly one year ago I started this blog with the main purpose of writing and sharing my experiences.

Nothing more, nothing less.

Then I started reading similar blogs on health, personal development and financial independence.

I noticed that Many Financial Independence blogs were publishing their revenues associated to ads, affiliated program and various products (e.g. eBooks, courses) etc.

Intrigued by this I started putting together something similar and…believe me…uniquely pushed by the curiosity that it is indeed possible to monetize the blog.

Well…to my misbelief you can and big time:

What I did

Amazon affiliates

Link to my favorite books and products.

After a couple of months of zero revenues somehow the revenues picked up.

Time to Set it up: 1h Average revenues per month at March 2019: $8,000

Adsense

I don’t like too much this method because it doesn’t give me a lot of control of the ads I am publishing but Hey…it works!

Time to Set it up: 1h Average revenues per month at March 2019: $$6,000

Ebooks

I wrote a couple of books (not big revenues here…I think I have to improve my writing skills). That’s also the item where I spent more time with smallest revenues.

COMMENTS

Not very active but I am not very surprised since:

1) Traffic is still too limited

2) Most of My blog posts doesn’t really leave a lot of room to comments, questions

3) I think people prefer to comment on twitter, facebook etc instead of directly on the blog

I am not surprised the Blogger Dilemma reached the top spot since with the proliferation of the blogs more and more people are somehow disappointed and disillusioned from the lower than expected traffic in their blogs. The post brings back on the basics: i.e. creating value. The post in second place very likely had several visitors trying to understand what the blog was about. I have to say I was not surprised of the post in third position since most of my readers seems attracted by topics such retirement, where to live and they are from the U.S.A.

In late November I started the Twitter account linked to this blog and I am having a blast to read all the interesting comments and post of my fellow bloggers out there. In few weeks I was able to reach over 100 followers (20% in my opinion are only real followers). I also opened a Facebook account linked to this blog but I do really think blog + Twitter is enough so far as main communication channel.

WHAT IN 2019

1) Publish every Saturday no matter what 2) Start some experiments in monetizing the blog 3) Extend to other social channel (e.g. Instagram, Reddit, Pinterest) 4) Being published by some media 5) Reach 10K Visitors/mo 20K Visits/mo

While always (trying to) create some value for you.

Many of Financial Independence Blogs rotate around a dogma:

The 4 percent rule.

Simply said and based on a study called the Trinity Study:

if you have a certain amount of money invested in a mix of stocks and bonds, 4% is roughly the maximum rate at which you can withdraw from the principal and being sure you will not run out of money.

Based on that dogma here another truth derives:

If you have saved 25 times of your annual spending …

Congratulations!

You reached Financial Independence.

(so hurry to give your boss your 2 weeks and your a well deserved Margarita right now!)

Why this dogma does not work

Life happens (and this is expensive)

The 4% is the max withdrawal rate…and perfectly matching your spending.

What about if you need to spend more?

Exactly.

2. Living in America!!!!

Most of the blogs talking about Financial Independence and Early Retirement are (curiously) based in one of the most unfriendly Countries for Retires: the USA.

Plainly said:

USA is one of the greatest place to make money while you are young, healthy and employed.

USA is also one of the greatest place to spend ALL YOUR money if you are not young, healthy or employed.

If you are sick and not insured (or under insured) in the USA you can easily spend thousands of dollars to treat a small health issue or all your capital…

The Trinity study and others of its kind have been sharply criticized, e.g. by Scott et al. (2008),[5] not on their data or conclusions, but on what they see as an irrational and economically inefficient withdrawal strategy: “This rule and its variants finance a constant, non-volatile spending plan using a risky, volatile investment strategy. As a result, retirees accumulate unspent surpluses when markets outperform and face spending shortfalls when markets underperform.” Laurence Kotlikoff, advocate of the consumption smoothing theory of retirement planning, is even less kind to the 4% rule, saying that it “has no connection to economics…. economic theory says you need to adjust your spending based on the portfolio of assets you’re holding. If you invest aggressively, you need to spend defensively. Notice that the 4 percent rule has no connection to the other rule—to target 85 percent of your preretirement income. The whole thing is made up out of the blue.”[6]

I become nervous…

Four percent might work…or maybe not…

Whatever…

Now what?

My rule of the thumb is pretty simply.

Align the percentage with the net return of dividend from Index Fund (as of today below 2%).

Why?

Because it is safe.

Because no matter what my capital is untouched and I have a good margin.

I am not an economist.

For the same reason why we all should invest in something more predictable with index funds tracking the total market and not try to invest in single stocks, we need to play with our money and life with a very ample margin.

Think with your head.

Be safe, even if this means retire few years later.

No, you don’t need that iron and plastic box sitting in your garage or parked (maybe far) somewhere in the street for seven reasons. I am going to show you 7 reasons why you don’t need a car…and if you really need it how to spend 10 times less than today.

Let’s turn on the engine.

Purchasing Cost

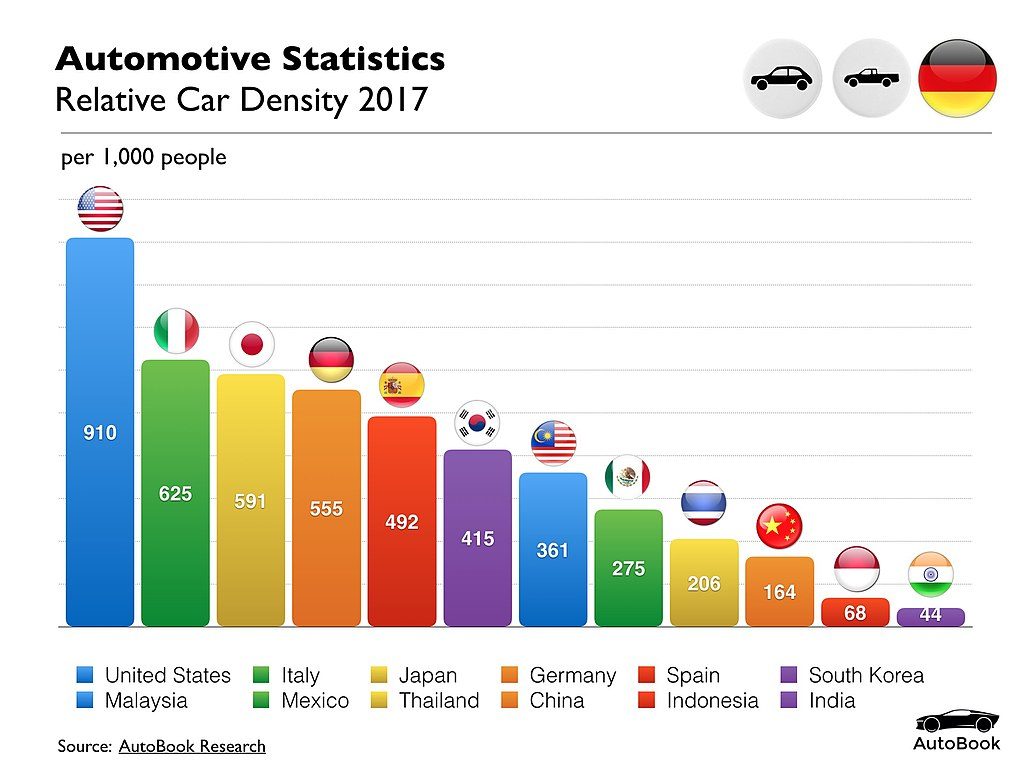

The Country with Highest Car density is USA (are you surprised?) with 910 cars every 1000 people. In second place there is Italy with a density of 625.

Highest Car Density in the USA…how surprisingly!

On average the cost of a car in the USA in 2018 is roughly $35,000 (there is a nice post of Financial Samurai on the cost of cars in the USA you can find here) .

Expensive…isn’t it? Let’s go deeper….expensive vs what?

How much a family is making in the USA, Italy or Spain per year?

Americans makes roughly $60,000 per year (before taxes…let’s say $45,000 after taxes) and (on average) spend $35,000 for a new car. Keep in mind these figures are averages…but they give a clear indications on the impact of owning a car.

Country

Average Car Cost

Average Salary after Tax

Car Cost vs Annual Net Salary

USA

$35,000

$45,000

78%

Italy

$24,000

$21,600

111%

The impact is devastating: Americans spend on average three quarters of their annual salaries on purchasing a car. For Italians one year of salary is not enough…!

In 2017 only in the U.S. more than 40,000 people died in car accidents, 110 every day! Car is one of the most dangerous place to be and full autonomous driving (i.e. no more human driving cars) is still decades away. People are scared of planes and lightening while they face dangers thousand of times bigger daily.

Health

On average Americans Spend an Average of 17,600 Minutes Driving Each Year…that is 293 hours. Almost one hour everyday… Add thisto the 8-10h sitting in the office and you have a more complete picture. Also consider that the posture and vibrations during driving have much worst effect compare to the office sitting

Pollution

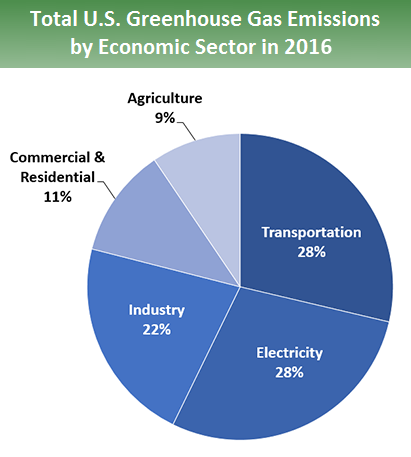

According to United States Environmental Protection Agency Transportation?, the transportation sector generates the largest share (nearly 28.5 percent in 2016) of greenhouse gas emissions. Greenhouse gas emissions from transportation primarily come from burning fossil fuel for our cars, trucks, ships, trains, and planes. Over 90 percent of the fuel used for transportation is petroleum based, which includes gasoline and diesel.

Impressive. Isn’t?

Additionally the dependence of fossil fuel created the (often negative) political dependence on the Country producing it. But you already know it…right?

You Simply don’t use it

How long do you think you use your car? 30% of the time? 20%?

What about 4%?

An interesting report found out that in Britain the average car is parked at home for 80% of the time, parked elsewhere for 16% of the time and is only on the move for 4% of the time.

4%…think about it…you spend tons of money for something you use only 4%.

Conclusions

Owning a car is one of the main negative think fro your finalce, heath and sanity. If you can’t really give up the metal box consider these alternatives:

Buy a use one: purchasing a second hand car can drop the cost of your car up to 40%, especially if you can find good quality used car (like in the USA)

Keep the car longer: don’t fall in the lures of owning the latest brand new car…for one hour pleasure you will have years of regrets. Buy a decent quality second hand car and keep it at least 10 years (yes I said 10…modern car can last in pretty good conditions more than 20 years)

Analyze the Alternatives Unless you live in a very remote area there are many alternatives to car: public transportations, biking, Uber (even thought for Uber the Risks of accidents are still there), walking!

You decide to buy and use a car. Acknowledge that…and avoid it if you can…

Joe was lucky…his parents paid for his college in a middle end university and for his used car (now ten years old).

John is very happy with his salary…a lot of money…

HR mentioned him about something called 401K and the importance of contribute to it…the company match..and the fact he is supposed not to touch it before 60 years….

Naaaahh this 401K is really complicated and looks useless and risky…then touching the money only when I will be 60 years old and very likely dead…? No Way!

So Joe starts his single life…

House $2,000/mo

Mhhh…the new apartments downtown Denver look very nice…$2,000 maybe a little expensive but…hey they are walking distance from all the cool bar an d restaurants of the area and you know I don’t want to move to a single family in the suburbs..I will do when I will be 40 years old and with two kids!

Bills (Electricity, Gas, Water, Misc) $150/mo

Joe is seldom at home, but when he’s there he wants to forget how cold is Colorado…!!! Luckily apart of electric bills he doesn’t spend much more on other utilities.

Car $1,000/mo

The 2015 Nissan look very old and crappy. I cannot leave in this suburb with this car and go out for a date with it…

Since now Joe is working credit is easy…so…what’s best than buying a new car especially now that there is a fantastic offer in the BWM dealer?

Put some gas, parking and Insurance…roughly $1,000/mo…no bad right?

Eating out $1,800/mo

Joe never cooked at home and his parents never thought him.

Anyhow there are so many restaurants downstairs for a quick dinner, Starbucks for breakfast and a great selection of salad bars around the office for a healthy lunch!

12$ Breakfast 18$ Lunch 30$ Dinner…not so bad!

Food Groceries $500/mo

Joe has no time and he doesn’t cook so he doesn’t need much food.

The upscale groceries store is just walking distance from his apartment

and hey..so many organic products!!!

500$/mo in so healthy products (too bad so many are thrown away because Joe is too busy and he forgets the expiration date)

Gym $99/mo

Mhhhh all that food and 8 hours sitting in front of the computer is manifesting big time on Joe belly…time to Gym..!

There is a cool Gym downtown…the price…a steal…all you can go open 24h and with swimming pool only $99/mo…!

TV – Internet $150/mo

When Joe come back he needs some relax..so what better than a 80″ 4K TV (5000K$) with a nice Internet + TV Cable + Netflix package for only $150/mo?

Mobile $70/mo

Joe has many friends right? So the unlimited data package at $70/mo is a must for his video call and social network…hey there are more expensive one…you know?

Furniture $30,000 (one time)

Having lived with his parents Joe doesn’t own practically anything…

and he has a 1200 square feet to fill now..!

Surely he doesn’t want cheap IKEA furniture in his posh apartment…besides he just discovered that in Boulder downtown there is a cool and trendy furniture store that import directly from Italy.

Wow…he has practically to buy everything…total expense $30,000…but it’s one in a lifetime!

Social Live $2,000/mo

Denver it’s so cool….! He cannot resist his clubbing, bar hopping and restaurant before Thursday (sometimes even on Wednesday)…

$500/week…well spent!

Clothes $150/mo

I really cannot go to work and in the club with the Ninja T-shirt I was using in the college…I need to dress like a young professional man now…Time to invest in my look!

Vacation $250/mo

Being a software engineer at XWZ tech Inc is very stressing!

Joe really needs to take a break from the cold of Colorado during his weeks off.. what’s better than hopping on a plane to Mexico or Hawaii…? $3000 really well spent!

Outdoor life Sky $1000 (one time)

Joe live in Colorado…he must learn how to sky…!

And so many people in the office go….

Here he’s with a brand new unlimited seasonal pass for only $999 (it was $1200…what a deal!)

Outdoor life Golf $50/mo

Well…with so many sunny days, great golf courses and many Managers and Directors playing in the company Joe must play golf during summer…poor Joe…with all the hours spent in the cubicle he really needs some fresh air

Health Care/Insurance $200/mo

Joe’s workplace offers a great Health Care package with only $150/mo from Joe pockets. Add a couple of visits for cold and small stuff (Joe is so young!) and the total cost is very limited.

The first year is gone…what a year!

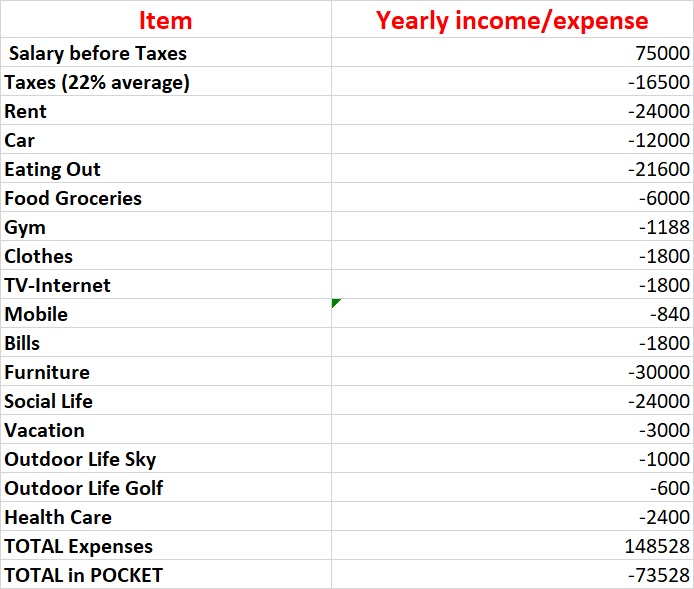

Let’s crunch some numbers

Ok…it was just the first year!

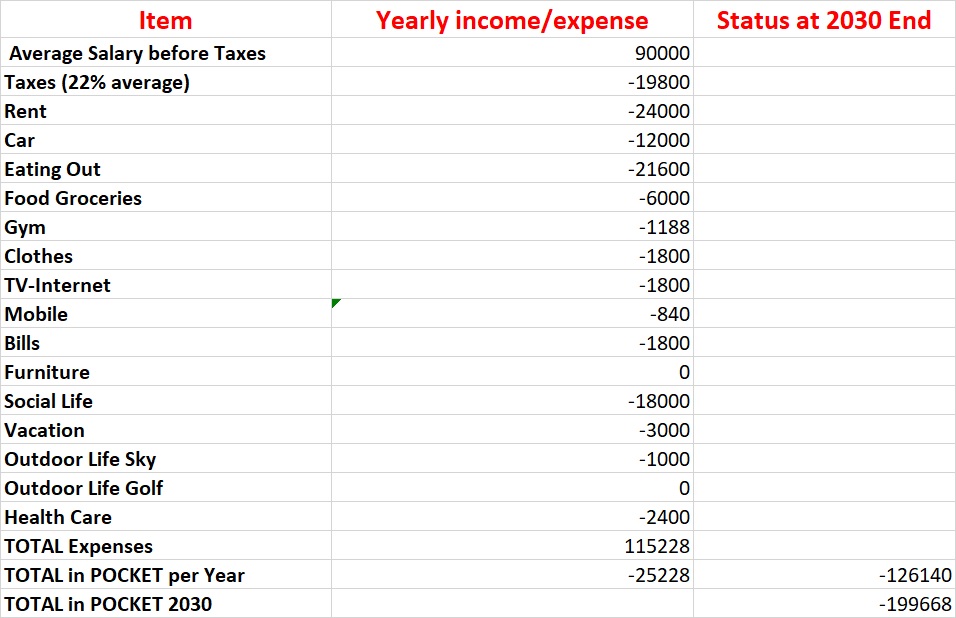

2025-2030

Joe had great 5 years as single guy in Denver.

The job was doing great…now he finally reached the six-figure milestone!

He also found a nice girlfriend and got engaged…thus the sweet single life is getting to an end soon.

Expenses wise he’s still doing the same life…just cutting off golf (too boring) and social life since he found a stable partner.

The good news is that Joe parents gave Joe (only child) their second home and he sold it for $250K thus so far no need of credit card debts.

Life is great for Joe!

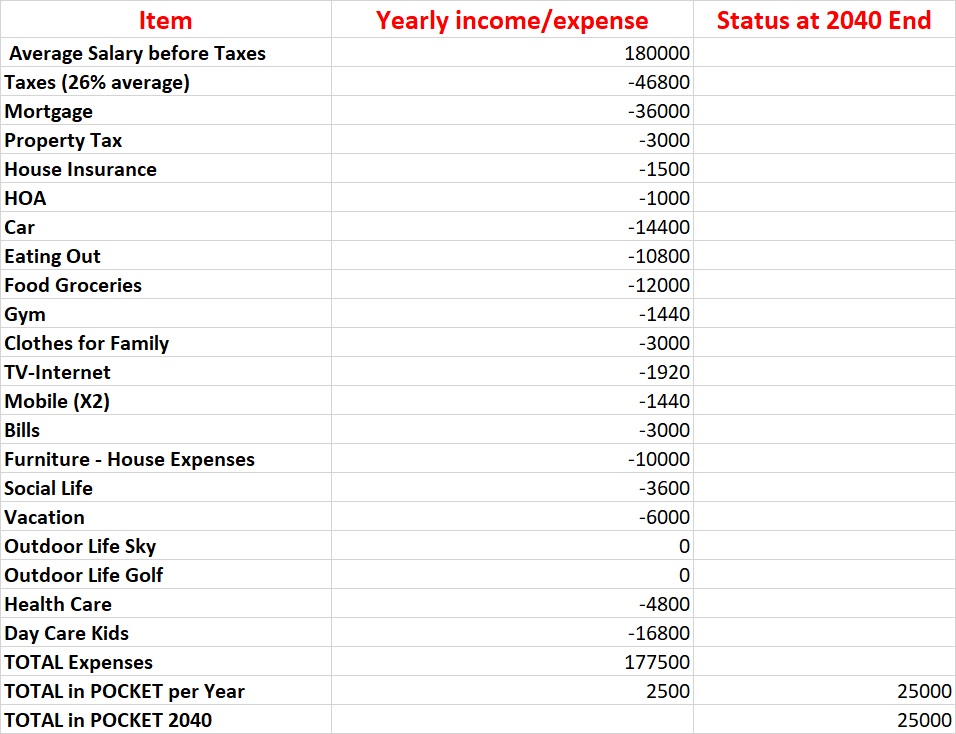

2030-2040

Joe gets married and two kids enlighten his family life!

Joe also get promoted as Director of Engineering in a new high-tech company close to Boulder and his salary and benefits dramatically increased.

Also the health care expenses increased with two kids in the family.

Kids also added day care expenses to the balance even though Joe’s wife is not working.

And of course a bigger family requires…a bigger house and cars ! (and vacation budget).

Luckily the social life expenses almost dropped to zero….

Here we are…

Some money saved at 40 years old…

Here it is Joe at 40 years old with some money in his bank….almost $25K…!

Joe feels almost rich with that amount available…now he can afford that vacation in Europe with the new 100″ TV or why not a boat or a new car.

$25K are a lot of money…isn’t ? Especially when almost of his peers are into deep debts…!

Of course Joe doesn’t want to hear about investing…he knows people talk a lot about Dow Jones, S&P, mutual funds…too complicated and surely a scam.

In any case Joe already made a great investment with the house…is not real estate the best investment around?

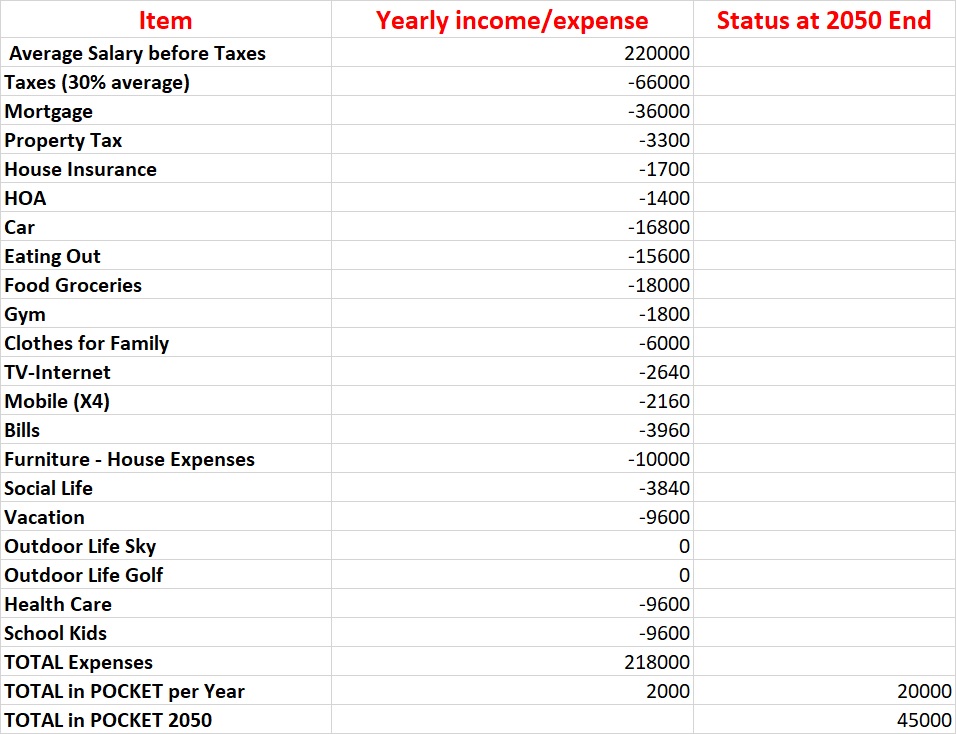

2040-2050

Kids are growing.. both are in High School now.

Joe got another promotion as Vice President of Engineer in a start up….those are the peak years of making money.

Savings are Increasing!

He’s happy because when he turns 50 years old he reaches 45K$ in saving (all of them in his checking account since he’s still not trusting the traps of investing!)

Also all expenses increased: Food (two big boys are always hungry!), Health care, Mortgage, Property Tax, Car Payments, Bills, Clothes etc but likely Joe is making great money…so no problems!

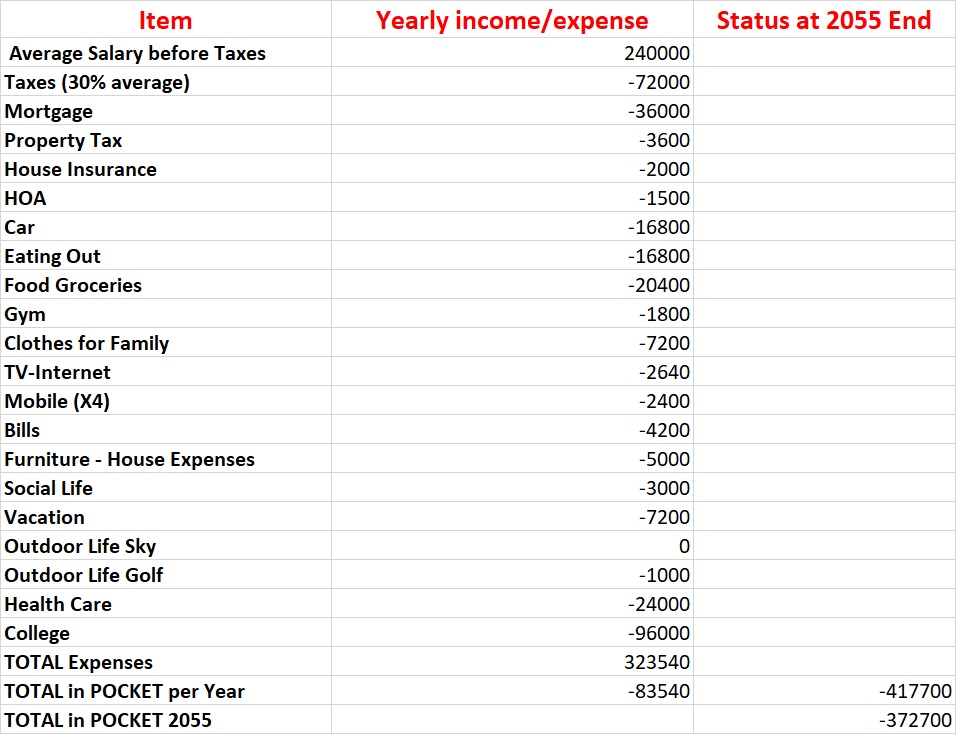

2050-2055

College years for the kids…both in an affordable one so the expenses are limited to $4K/mo per kid…all included (no bad right?).

Health care expenses are going up…Joe and his wife are both in their 50 and co-payments and dentists expenses increased and the kids are still on their insurances plan.

Joe started again with golf thinking about retirement…

Economically the situation started deteriorating…not only Joe spent all the saving but now he has almost $400K debts at 7% average in college loans and on a couple of credit card.

College years…

2055-2060

Joe and wife don’t think downsizing from a big house (now empty since the kids left) and luxurious European care is a wise move.

After all they are affluent middle class right?

Joe was caught in a sudden layoff due to economical crisis and, as usual, the highest paid are the first to go.

He stay almost one year out of workforce and he found a job as Manager R&D with a substantial pay cut.

Luckily the kids are practically out of college and all almost all the expenses of Health care are for him and his wife.

Unfortunately their expensive lifestyle is costing more than Joe salary…roughly $50K are going into credit card debts per year to compensate the expenses.

It will go better now with kids out of college!

Debts are increasing

2060-2065

Joe job is stable and kids finally are paying some of the college loan back.

Great news…no more mortgage and Joe finally decided to buy a slightly less expensive car.

All the other expenses are going down as well apart the health care since they both went under a couple of surgeries and therapies.

They were able to save more than $100K in five years…not enough to finish to pay the debts…

Some savings are back…

2065-2070

Joe retired.

Between Social Security and Companies pensions is bringing home $50K before taxes.

As we know Joe never believed in investing or 401K so the $50K before taxes is all they have.

Kids kept giving the money back for the students loans but in 2070 they repaid everything and now they have their own family to take care of.

Joe and wife are roughly more than half million dollars in debts.

The retirement

2070… and the future

So what now…?

Joe and his wife now are forced to downsize the house and giving up the expensive cars.

Doing so they are able to reduce their debt to $300K in 2072.

Too big anyhow the debt (at 12.5% interest on 5 different credit cards and one home equity) to be repaid.

Joe and wife will likely die poor in some hospice giving as gift the debts to the kids.

This is no fantasy

Every year thousands of people end up like Joe and his wife; despite making a great salary while young and having his parents paying his college.

Every years people cannot realize they are spending more than what they make and that they need to save money for the future.

This is no fantasy…this is the sad typical middle class life.

Ok…let’s start with the definition (thanks Wikipedia)

…that retailers traditionally operated at a financial loss for most of the year (January through November) and made their profit during the holiday season, beginning on the day after Thanksgiving.[7] When this was recorded in the financial records, once-common accounting practices would use red ink to show negative amounts and black ink to show positive amounts. Black Friday, under this theory, is the beginning of the period when retailers would no longer be “in the red”, instead taking in the year’s profits…

So…what’s the link of Black Friday with big sales and the push you to spend…?

Nothing.

Just another day created to make you waste your hard-earned money (like Christmas, Valentine day, Mother’s day, Father’s day, Teacher’s day, Your Neighbor day (last one I made it up but I am pretty sure they will invent it soon).

The word today is:

RESIST RESIST RESIST!

Yes…like him

Why? 5 Reasons…

1 You save 20% to spend 30% more

Black Friday is a big, fat bait.

Attracted by the 90% off Laptop (that most of the time gets sold in 5 minutes) you enter in the store (online or offline) and…voila…you exited with ten objects that you absolutely didn’t need it but you bought them just because they were 40% off…! (tell me the truth…how many memory cards or disk dusting in your drawer do you have…?).

2 You can find better deals

Make an experiment…just check the price of a product during the Black Friday Sale…the regular price when it’s not on sale and track the price during following 6-8 months after Black Friday.

You will be surprised…

If you don’t want to wait just read this study from NerdWallet:

In a NerdWallet analysis of 27 Black Friday advertisements, 25 retailers listed at least one product for the exact same price in 2014 as in their 2013 Black Friday ad. That means 93% of retailers are repeating Black Friday products—and prices—from year to year.

Surprised, right?

3 You are going to buy old stuff

Yes..yes…the brand new TV is 80% off but very likely they have only 2 in stock!

The rest of the items are older items (usually the previous year) that will be on sale anyway.

You will end up buying this one…

4 Black Friday Day last more than one month

Already in the end of October we start seeing the Black Friday month deals…then the Black Friday day deals… then the Black Friday day deals…then the Cyber Monday deals…then…the Christmas period sale…then the New Year day sale…

If everything is always on sale every time…where is the deal?

and move to a Caribbean beach or in some countryside in Europe and maybe open your small bar, business that (of course!) it will be very successful…bla bla bla….

Or…join the latest trend of movement of FIRE (Financial Independence. Retire Early)

SO… (did you notice how big was this so…?)

Why you didn’t retire yet?

You know…the kids, the mortgage, the family, the <enter other excuses here>…”

Ok, let’s see why you didn’t do it yet and why you should change right now your approach on this for your mental sanity.

Now the second part of the question…the most difficult

Retire to do what…?

I am hearing you less now….some weak and general statements like………

To golf more

To sleep more

To spend more time with my family

To relax

To read…write…

To play an instrument

Your answer

So…if the reasons above are so strong to make you consider to quit your job and changing radically your life…why don’t you dedicate more time to them while you work…?

If playing golf is such a burning desire…why you are not more efficient with your time (e.g cutting internet/social media/TV time) to satisfy that burning desire?

Same for the rest…

If you are not spending time to do the things you think you like it’s only because there is not a burning desire behind them.

Instead you decided to waste your life watching a screen instead of living it

You just want to retire from something to…become lazy!

Wasting time in front a screen is your burning desire…

Let me repeat….

Wasting time in front a screen is your (only) burning desire…

Because you do it day in-day out for hours and hours and you are never bored doing that…

Indeed with the advent of the smart phones and tablets we are not bored anymore because we have anyhow always something to do…watching our phone!

Help me…! What should I do then?

Assess yourself

Shut down all the distractions and ask yourself what you really like

The goal here is to really understand your passion once you remove the screen time…(use phone app or other tools to track it)

You used to like golf, swimming, playing guitar, bla bla before the screens came in the picture… right?

Reignite again your passion

Start practice again what you use to love.

Set a schedule calendar for it and do it

Enroll in some tournament, competition, to set a measurable goal and a target.

It would be strange in the beginning but you will rediscover the desire…

Act on the big dream

Leaving in Europe opening a small business was your dream and 9-5 escape ?

Start planning it.

Plan a trip THIS YEAR, discover how to buy/rent a place over there…if that’s the place you really like…start thinking about the business.

You decided to invest your time reading this blog instead of watching TV or mindlessly browsing your phone…so you are committed to change, clever, energetic.

You can do it…no doubt about it…start now

That’s it.

Few points and actions.

We make it complicated but it’s not.

We just lost sight of what we are and what we love

Understand that the world out there wants every second of our attention to MONETIZE it…

Don’t fall in the trap, you are more clever than who wants to suck your money and life

Saving enough money so that the passive income generated will cover all your expenses

We already talked about saving…what about passive income?

Passive Income

Passive income is the ultimate goal and dream….a vehicle that generates money 24/7 no matter what we do (sleep, golf, watching TV) thus the name passive.

Being paid to do what you like, no boss, no alarm in the morning, no customers…no bad right?

Now the question is how to build this vehicle, this mountain that will generate that lazy flow of money

Let’ s look again at our options…

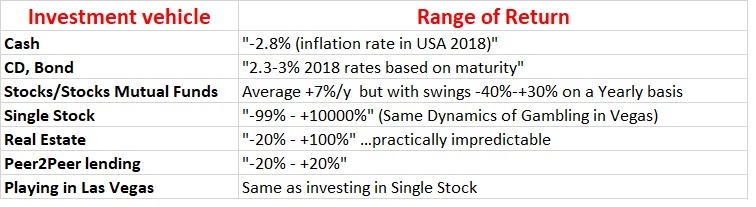

Cash

While it’s good to have cash it can only lose value in time due to inflation.

Keep max 3 months of living expenses in cash and put it in some high yield checking or saving account that you can access instantly.

Period.

Don’t keep your cash in a suitcase!

CD-Bonds

Safest passive investment and because of it with the lowest return, barely matching inflation. You can make a little more money with municipal bond or bond fund with a little extra risk.

Despite the low return bond should be an important portion of the invested portfolio; the closer you are to retirement the highest the portion you should keep in bonds since it’s better during retirement not to have all portfolio allocated in stocks because a recession can eat up a big portion of your stocks portfolio and you might not have the time to recoup it.

In the USA the Bond yield typically track the interest rate of the period and the longer the maturity the higher the yield (unless the economy is closer to a recession and the yield curve is flat or inverted)

Investing in a CD insures that you will get your capital back plus the promised yield at the maturity

Example

If on Jan 01 2010 I invest $10,000 in a 1 year CD offering an yield of 2% on Jan01 2011 I will get $10,200 (the initial $10,000 plus $200 (2% of $10,000))

Stocks Mutual Funds There are thousands Stocks Mutual Funds over there, most of them too complex to understand or designed in a fancy way to attract you and charge you expensive fees.

Forget about the products your banker is trying to sell you and go for low cost (<0.05%…even better 0 now from Fidelity) index fund that tracks the major index (like S&P 500 or FTSE).

Depending on where you live, check with your bank or financial services provider and go for it.

Again watch out the fund fee…you must select a fund with less than 0.05% fee per year (basically for $10000 invested you pay $5 year).

If you are an absolute beginner my suggestion is to invest 80% in a passive managed low cost index fund that track total market stock (USA or European) and the remaining 20% in an as well a passive managed low cost index fund that tracks the total market bond (USA or European).

If you have some form of pension tax deferred (like 401k in the USA) where your employer matches your salary contribution (1-5% typically) maximize this first, than maximize IRAs and only after invest in taxable accounts

Never ever underestimate tax and fee…they can wipe out your return or even worst making it negative.

Individual Stocks

The Las Vegas for stock pickers.

I have to admit, I sometimes picked some single stocks, allured by the name or the buzz around it.

You don’t want to pick single stocks

Always remember,

You are not a stock expert and very likely (excluding Warren Buffet there are none around).

Why? Because you don’t have all the information about a company to be sure your investment is solid. One legal problem with the company you invested or government changes some rules and your stock can lose 20-30% in one day Have you ever imagined 20-30 years that company like Kodak or Nokia (add stock graph) could disappear? N(stock chart) I didn’t so who place all your money there lost everything.

To use a dramatization Think about on investing in a single stock like betting on one number in a roulette…big win if the stock soars but also high risk of lose everything.

Think about investing in the stock market through index fund on regularly betting some money on the red in a casino where red is slightly more frequent than black or zero

You will surely face temporally lose but on average and on long time you will make some money (chart stock s7p or dow)

Real Estate

Real Estate can be all you need to have a solid Passive Income

It can be a good, bad or disastrous investment.

To minimize risks:

Rule#1: Location Location Location

Even thought it’s not certain, buying in downtown New York or San Francisco or in front a prestigious campus means buying a property with some intrinsic value.

Same for an oceanfront property or one close to a prestigious landmark (an apartment with a perennial obstructed view on the Eiffel tower).

I understand few people can afford this properties, foe the rest of us just do your due diligence, look for places with a healthy job market, universities, landscapes.

Look for unique features , be sure the competition around you is limited (e.g., no more buildings are allowed) .

Talk with trusted realtors, ask for data on comparable sales in the area and average rental (and average vacancies as well)

Study study study

One rule of the thumb says you should get 1% month of the property value per year in order to have positive cash flow (e.g. $2000 per month if your purchase price has been $200,000).

I find that nowadays getting 1% is very hard unless you were fortunate enough to get an excellent deal on the property or investing in some rural Midwest property during an economical expansion (but watch out at what might happen during an economical downturn to those properties).

In mature areas I find that 0.55-0.65% are more common rates during the first 5y of ownership with gradual increases.

Anyhow Real Estate when well purchased, financed and maintained can be a great investment in the long term and a good edge against the inflation since both the rentals and the values on average growth with the inflation.

Besides, based on where you have the property you can have great tax deductions increasing your ROI.

Peer to Peer Lending

A relatively new investment.

There are two kind of lending through an intermediary (usually a company with a website)

You basically act as a bank, landing money to privates (or small companies) for disparate investments from buying a car to invest in a multi-million dollars projects.

Of course the higher the risk the higher the return

Based on the country you reside you can also have detailed information about the borrower such as his credit history and based on this information the intermediary will fix the interest rate to charge him.

You can thus decide to lend money to high quality borrowers (who wants to keep that status to be able to access cheap credit) but a low interest rate or the opposite (to high risk borrowers thus charging higher interest rate)

Up to you…I personally prefer go for a mix to minimize my risks but at the same time getting some more return vs Treasury bond or other means of investment.

Still Confused? Don’t have to! Keep it simple

That’s all… and believe me it’s not so complicated like our banks or “financial advisors” want us to believe.

Don’t think investing is for Wall street gurus and complicated and the only way is to buy useless and very expensive managed mutual funds from the “financial advisors” with lower return vs the market.

Don’t overlook the importance to invest some money and time to maximize tax return, or to avoid to buy everything full price.

Believe that many people reach financial independence simply saving more money and investing wisely the difference.

Believe that there is an alternative life vs living paycheck by paycheck out there if you just want to chose it.

Overall, 71 percent of all U.S. workers said they’re now in debt, up from 68 percent a year ago, CareerBuilder said.

While 46 percent said their debt is manageable, 56 percent said they were in over their heads. About 56 percent also save $100 or less each month, according to CareerBuilder.

On this subject people, especially in the USA, discussed and are discussing ad nauseam.

But still people seems not getting the importance of it, or simply don’t care.

And this is happening in the richest and most developed economy of the world.

Why?

Mindset and Ignorance .

Let’s analyze, change them and get the first step towards Financial Independence.

Let’s start with mindset.

Mindset

Western society are based on capitalism that in the last 60-70y (let’s say after the end of WW2) degenerated in the concept of need of constant growth and increase of consumption to sustain the economy.

The concept of the constant growth is a pillar of modern economy.

Economy Growth as increase of the market value of goods and services.

Basically every company should grow in order to make more money, so increasing the market value of goods and paying taxes, the services of the Country where they operate.

The concept of strong economical growth at Country level is fundamental in emerging economies where it’s urgent to reduce poverty and build basic infrastructures such as roads and access to basic services like drinkable water, electricity and gas.

Conversely in developed Countries the continuous grow became a boomerang i.e. decreasing the quality of life of people for low/no returns.

That’s where we lost happiness to get almost nothing in change.

In a nutshell: being stuck three hours in traffic to work and contribute to economic growth in a third world emerging country might be worth if I am going to use such hard earned money to feed my kids, have clean water in the house or a roof under my head.

But (and this is a HUGE but) if I decided to be stuck in traffic in L.A. or San Jose mainly to pay the mortgage of my 4000 square feet (where I am not very often anyhow because I am always at work to pay the mortgage!) or the loan on my new cars or the latest cell phone, camera, luxury gadget etc. is very different.

We need to spend the money (as result of the growth) in something that improve our lives as total balance.

If, in a scale 0-10 (with 10 meaning full satisfaction) working is reducing my lifestyle let’s say by 5 points but what I can buy with the earned money is increasing +8 (to feed my kids or having clean water in the house etc) the balance is positive. (-5 +8)

Conversely if a bigger mansion or the new “toys” give me back 2 o 3 point of quality life there is something wrong.

Let’s take the car for example

Well..maybe a little newer…

I had several discussions with friends making 1300-1500 USD (or Euros) per month on this subject.

I show them that, using a conservative calculation, an economic car (purchase price, repairs, insurance, tax, gas excluded) costs at least 1000-1500USD or Euros PER YEAR.

This means that they work one full month ONLY to have a metal box with the wheels on the road that they use it….90% of the time to commute to a job!

So… I need the car to go to work and I need to work to have the car…can you see something strange here?

You might think, there is no solution, I need to work and I need the car… are you really sure?

Did you consider all the options?

Like using public transportations? Moving your house closer to your job or …biking/using a cheap scooter to go to work?

Or, if really having the car is a must, what about to buy a cheap, low consumption and used one and keep it for ten or more years ?

We are so blinded by the mantra find a job, spend your money, pay your bills and die that we don’t even realize what we are doing.

Every penny spent needs some work to do in order to earn it and this work needs your time that you will not be able to spend with people or doing things you love.

Think about it, every time you spend money think in term of time needed to earn it, time staying with people you might hate, maybe your boss, your coworkers, your customers doing a dull and stressing job.

Our mindset should shift from “We work because everyone does it” to “We work in order to be happy”

Happy because our job is IMPROVING our life either like in the case of the person living in the developing countries or if working is satisfactory or if the money are good enough to aim to a quick financial independence.

Ignorance

People live paycheck by paycheck because they ignore there is another way of living.

Clear, simple and dramatic.

They make 10 and they think they are entitled to spend 10 (or 12 or more especially in the USA where paradoxically everyone should be very rich compare to other places in the world ).

The solution? Financial Independence

The only way out that is saving to reach Financial independence (FI) like we already discussed.

The formula is very simple:

If

I spend each month $XXXX

I am able to generate revenues from passive investments (rental income, side job, dividends, blogs, etc) $YYYY

If $YYYY is ALWAYS equal or greater than $XXXX I am financially independent => I don’t need to work a single day in life anymore.

Everything boils down to three numbers:

1) How much I spend each year ($XXXX)

2) The net worth I have that generate the passive income ($YYYY)

3) The interest rate of the net worth that generates the passive income (Z%)

As said the FI is reached when

Expenses <= (Equal or less than) Passive income

Being

Passive income=Net Worth * Average interest generated by the net worth

We have:

Expenses <= (Equal or less than) Net Worth * Average interest generated by the net worth

Let’s make a practical example

Yearly Expenses=$24,000

Net Worth = $1,000,000

In this scenario we need a net interest of 2.4% ($24,000/$1,000,000 * 100) to cover the Yearly expenses

If our net worth is $2,000,000 we would need only a net interest of 1.2%.

Intuitively if we reduce our Yearly Expense to $20,000, we need a net interest of 2% ($24,000/$1,000,000 * 100) to cover the Yearly expenses

If our net worth is $2,000,000 we would need only a net interest of 1%.

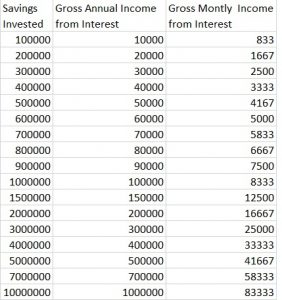

Let’s examine some scenario

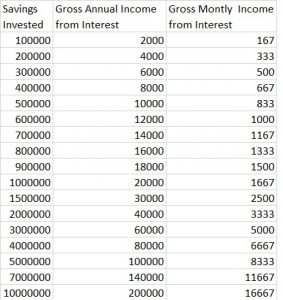

Gross Income with 2% return

To get $24,000 per year with 2% return we would need $1,200,000…with $5,000,000 saved we will net $100,000per year before tax…with $600,000 we can afford a $1000/mo lifestyle.

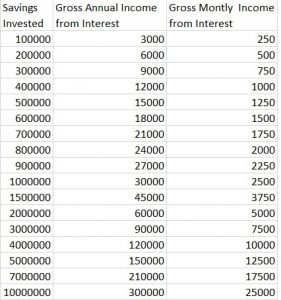

Let’s see what happen when we bump our saving rate to 3% – 5% – 7% – 10%.

Here it is the gross income with 3% return

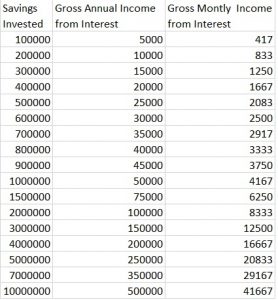

5%

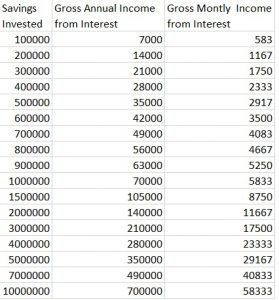

A juicy 7%

An incredibly handsome 10%

Thus Making, Spending and Investment Return is all what you need to know

1) Making

Making is the active action of making money i.e. you are doing some actions to generate that cash and if you stop doing it that cash flow disappear almost immediately.

Typically the sources are:

1) Your primary job (9-5pm or entrepreneur)

2) Side job (selling stuff, blogging with revenues, uber driving etc.)

3) Passive Income from Investments (dividends, royalties, real estate rents, peer2peer lending etc.)

Usually you know what’s the average income you can get from these activities, let’s forget for a while the possibility of inventing a great product that will skyrocket your income and let’s focus on your average income.

You know what you are making but maybe you are under evaluating how much you can increase your income.

Typically (unless you are already in a high expense area with well above average salary) you can double your income simply changing job description and/or Country.

Yes double.

I know several people (me included) who doubled or tripled their salaries simply changing function or more commonly workplace.

But guess what…?

Not so many…why?

Because People are resistant to change

They prefer 40 years of paycheck to paycheck agony vs 10-15 years maybe far from home or in an unconformable job but with a solid income and reaching a financial independence.

Comfort and agony….if we add no tight expense control to equation you are doomed to 40 years of mediocre job and life. You might be happy, sure, but honestly today I found that 90-95% of 9-5 people are complaining about their job, peers, boss etc. and their hobbies, vacation or family time is never enough to compensate the 80% of the time they spend for job related activities.

Being happy while you spend almost all of your low income is not the pathway to happiness…we know that…

So….what should we do? Changing radically our job or location?

Yes (in case you missed it this was a big yes…)

Listen, if you are lucky maybe you don’t have to change location but it will be almost impossible to double your salary remaining in the same industry and region (unless you are enslaved in the actual one).

One alternative is to change industry and move to a better paid one. You might need to go back to school and get more skilled for that.

Or get skilled on making money on the internet flipping stuff or blogging or become an influencer in something

Whatever it is you need to take BOLD actions.

2) Spending

This is the easiest part, believe me.

I am already hearing you “come on man…I am already cutting corner everywhere…where can I find that extra $10!”

Are you sure?

Do this exercise for me.

Track every expense for a month (to the dollar, euro, rupia, yen, rmb…whatever else) and analyse it.

Are you still sure you cannot reduce eating out so often? Or using that car? or cancel the expensive subscription you never use? Or reducing wasting food?

Or not buying the thousands of expensive and useless gadget? Or in vacations?

Yes you can and you must to reach FI.

Reducing expenses is much important than revenues because it has a double effect: for every dollar saved you reduce the money you need to reach the financial independence AND you can invest that dollar that will produce passive income

3) Investment Return

That’s the tricky one, especially if you are not skilled in investing.

It’s intuitive the fact that higher is your Return on your investment (or Yield) higher is your monthly check from the investment…but what is high and what is low?

The easy part…Higher the risk higher the return

The difficult…find a sweet spot between risk and returns

There are 3 or 4 way of investing after tax money…here they are

Rate of returns…

Confusing…?

I bet it is but it might be much more simple than you think…

What’s next

In next post we will go through these difference way of investing…for now just keep in mind that the solution is simple: saving enough money so that the passive income generated by your investment will cover all your expenses.

This is call Financial Independence, i.e. you are independent (free) from working to have your finances covered

To most of the people Financial Independence is like a dream….something not real…something only for very rich people.

Whenever I talked about it most of the people dismiss me with a gentle “whatever“, like I told them they only need to win the first price of the lottery tomorrow to make it.

These are the same people who live a miserable life of paycheck to paycheck slavery…I wonder if there is a connection…

But if reach the end of this post you will not end up like with those people.. I promise you…just wait for next post…